Powered by

⏱ Avg. Reading Time: 6 min

The desert has been inspirational for many people throughout history. It is considered a place where nations were established, and legends were created. Throughout the years, the desert was seen as a land of opportunities – free from influences or intervention. Yet, history has shown that creating sustainable livelihoods is very challenging in an area where climate is extreme, water resources are scarce, and fertile land is limited.

More than two billion people live in deserts and drylands, which cover approximately 40% of the earth. As these numbers continue to rise, so too does the urgency of developing technologies to ensure food and water security. Hosting one of the world’s leading DeserTech ecosystems, Israel is one of the only countries in the world that has managed to reverse desertification by developing innovative solutions that enable sustainable living in an arid climate. As a result, Israel attracts leading scientists, environmentalists and solar energy enthusiasts seeking to learn from and replicate its success in the fields of sustainable energy, water technology, and AgriFood-Tech. Israel has a central role to play in tackling this potential humanitarian and environmental crisis, particularly in partnership with other countries that have a similar climate and thus similar climate-related challenges.

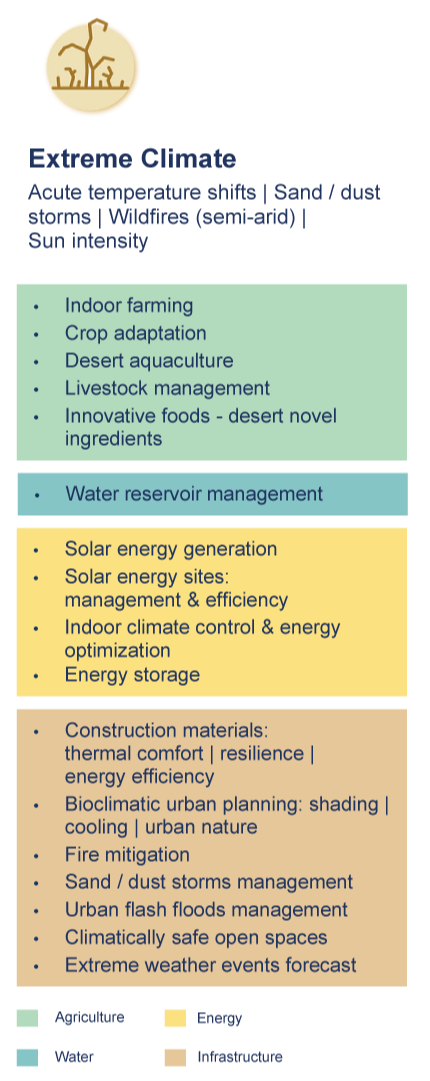

Dust storms, droughts, heat waves, and flash floods are all intensifying environmental threats for desert inhabitants. As desertification increases, agricultural productivity, and income decrease. According to the IPCC Special Report on Climate Change and Land, extreme weather events have the highest potential to increase poverty over the coming decades in dryland areas, urgently necessitating innovative solutions to ensure food security and alleviate poverty.

Heat and dust resilient renewable energy sources, green desert construction, adapted agricultural crops, sustainable land management practices, and prediction systems for extreme weather events are just a few of the solutions needed.

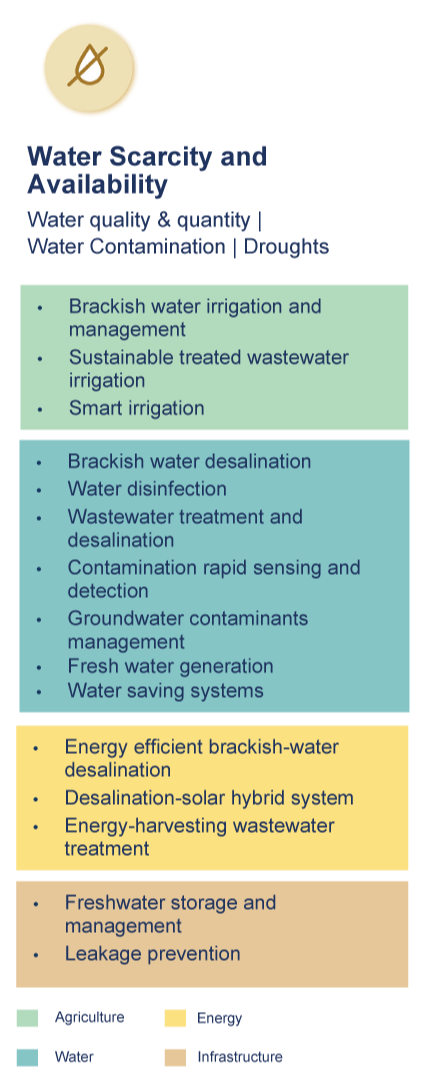

Prolonged droughts and soil degradation will continue to aggravate existing water scarcities rendering life in the desert even more difficult for its inhabitants. Climate change will exacerbate water shortages, negatively impacting regional agricultural systems. By 2025, 1.8 billion people will experience "absolute water stress," threatening water security worldwide, especially in arid regions.

Desalination-solar hybrid system treatment, reuse and treatment of wastewater, water-saving precision irrigation, generation of water from air humidity, and advanced systems for drought forecasting are just a few of the solutions needed.

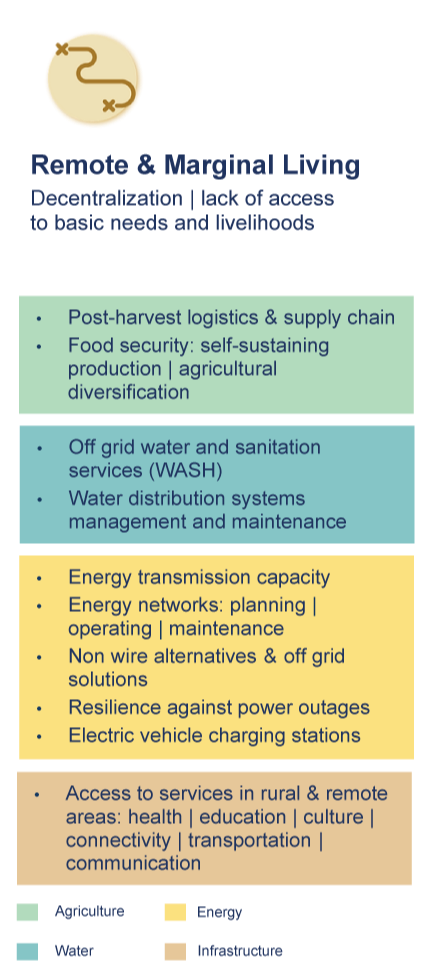

The lack of food and water security, reliable clean energy, and access to basic healthcare all test the survival of communities living in remote arid environments. The desperation of people living in these drylands is likely to drive them to emigrate leading to additional challenges for the global community. As desertification expands, marginal communities in arid regions will only be able to thrive with the use of new technologies. As of 2019, more than 785 million people in the world did not have access to basic water services.

Off-grid water and sanitation services, non-wire clean energy sources, and innovative self-sustaining food production technologies are just a few of the technologies needed.

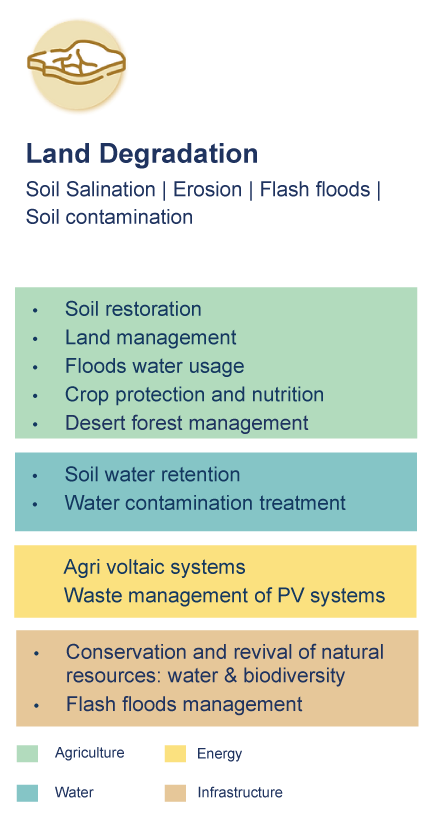

Land degradation is primarily the result of human-related activities and climate variations. When land degradation occurs in drylands it is considered desertification. Unsustainable land management practices and increased pressure on the land to produce combine to drive degradation. Every year, 75 billion tons of fertile soil is lost to land degradation, thus increasing soil vulnerability to water and wind erosion, salination, and flash floods.

Land management techniques using runoff water, soil restoration, agro-voltaic systems, and smart irrigation are just a few of the solutions needed to achieve land degradation neutrality.

The data in the report is updated to March 4th, 2022.

Definitions – DeserTech verticals and solutions definitions were specifically formulated for this project. All other definitions including Funding Stage, Financial Maturity, etc. are taken from the Start-Up Nation Finder glossary.

The companies that were included in the mapping were founded from the year 2000 onward.

Capital raised information in the graphs usually refers to rounds and amounts raised since 2014. The total funding raised by the sector and by each vertical refers to 2006-2022.

As a result of the delay in collecting data on company foundation and funding rounds, the information associated with 2022 is partial, both in terms of the number of companies and the amount of capital raised.

In terms of technologies designed to adapt to desertifying environments, Israel is no stranger to the problem as it had faced these challenges since its establishment with its settlements in arid and semi-arid zones which required appropriate solutions. Solutions that focus mainly on water, agriculture, and energy have formed the basis for the establishment of technology startups that operate in these fields.

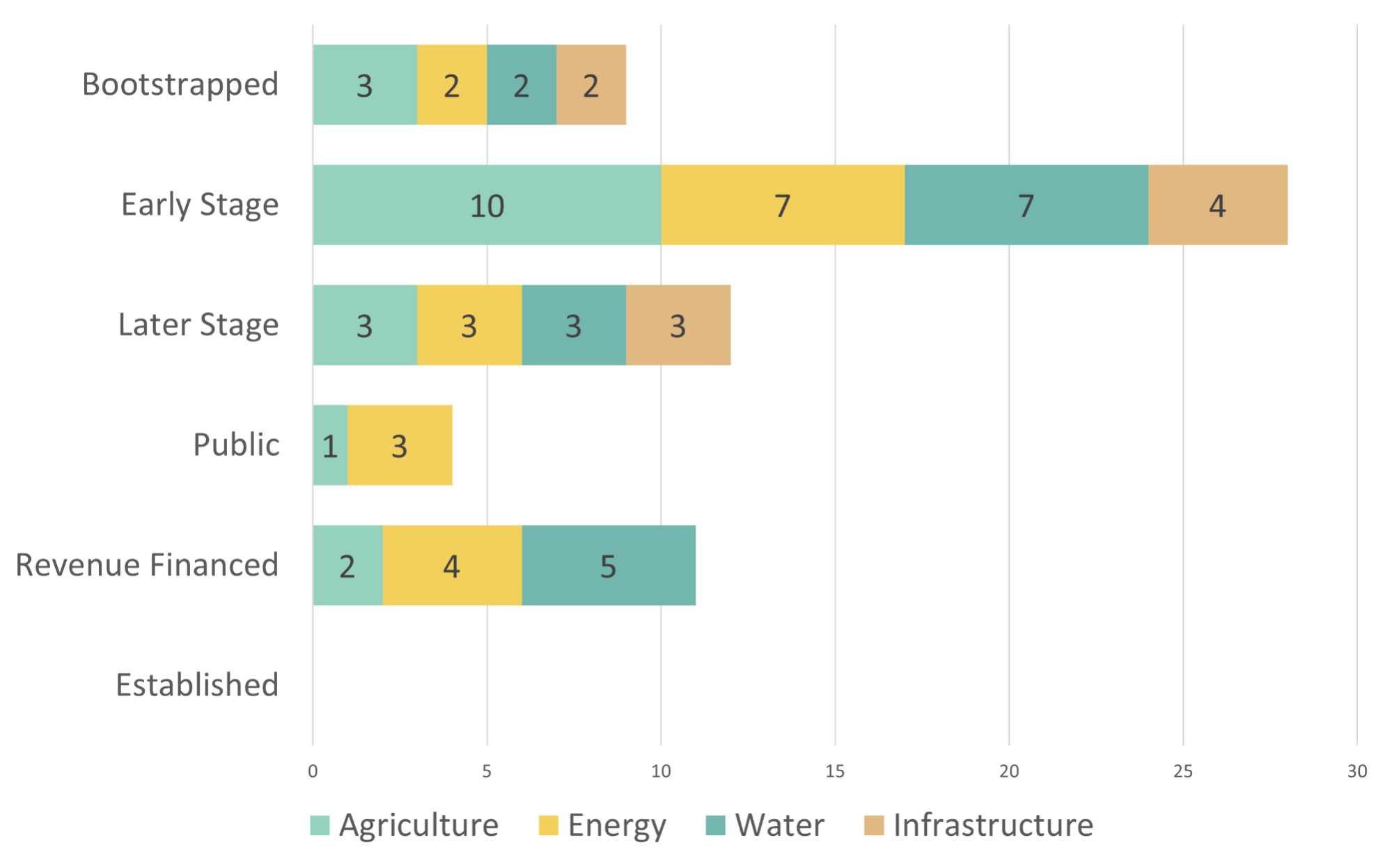

There are currently 66 startups dealing with desert challenges, distributed relatively evenly among four verticals: Agriculture, Energy, Water, and Infrastructure, with the last vertical having only half as many startups as the other three.

The number of startups in every vertical except infrastructure is realtively equal.

Figure 3.1: Breakdown of Startups by Vertcial

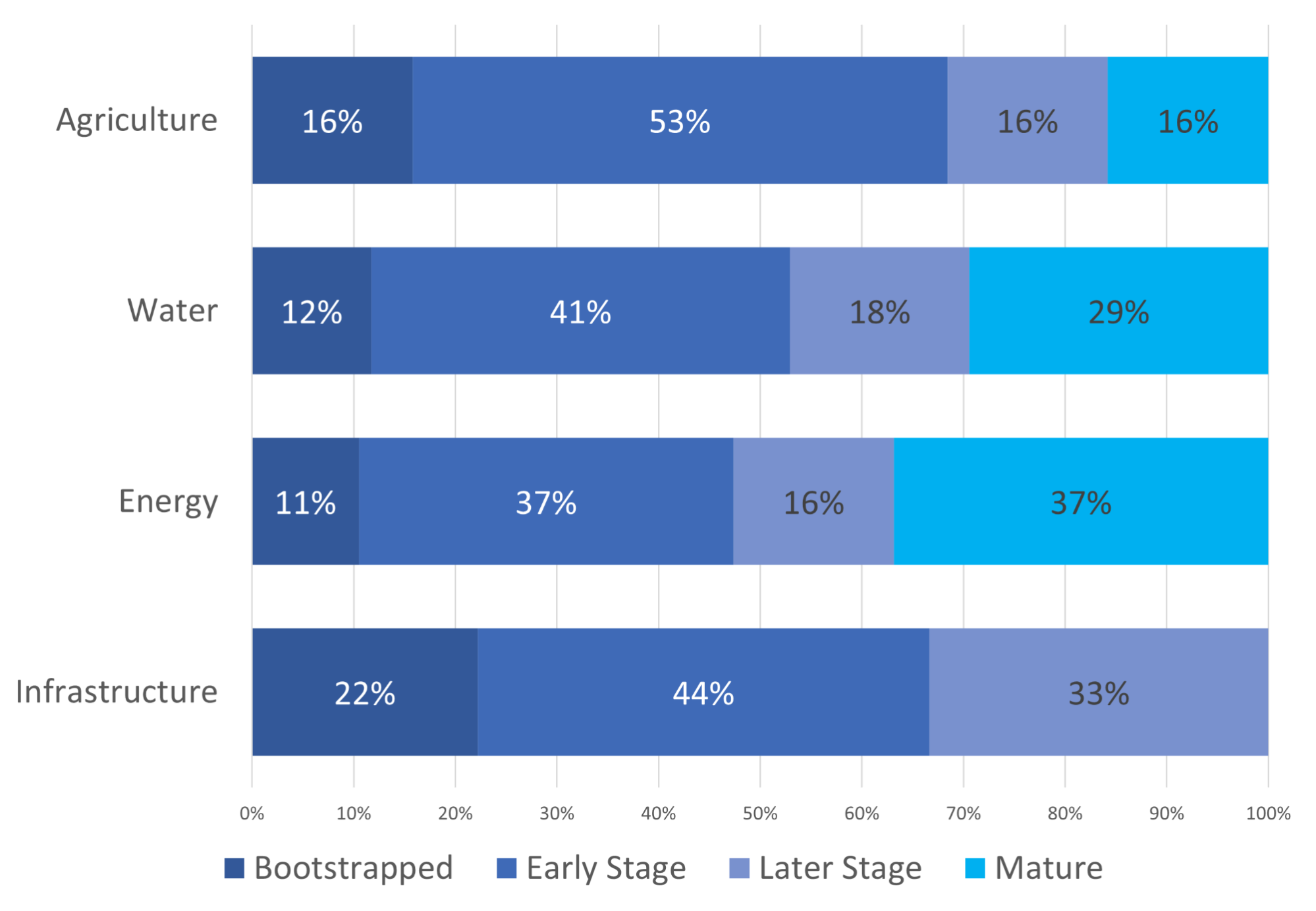

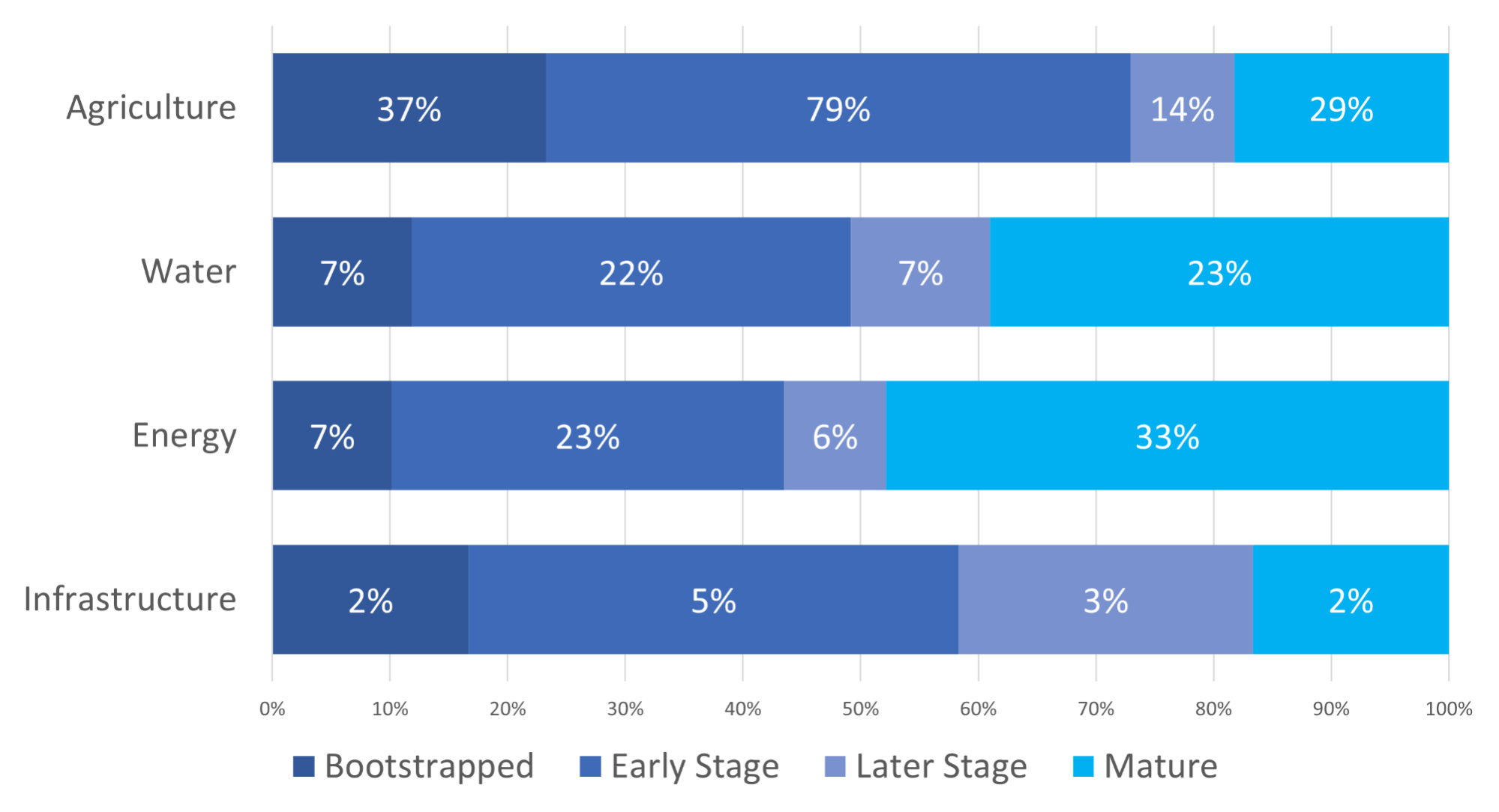

The majority of startups are in their initial stages, with around 60% of them bootstrapped and at an early stage, with agriculture and infrastructure having around 70% of their startups in these stages, and water and energy having 50%. Thus, it is expected that 'future companies' will mainly address challenges in the agriculture and infrastructure verticals.

Agriculture and Infrastructure are less mature verticals and most startups are in initial stages.

Figure 3.2: Distribution of companies’ maturity levels by verticals and stage

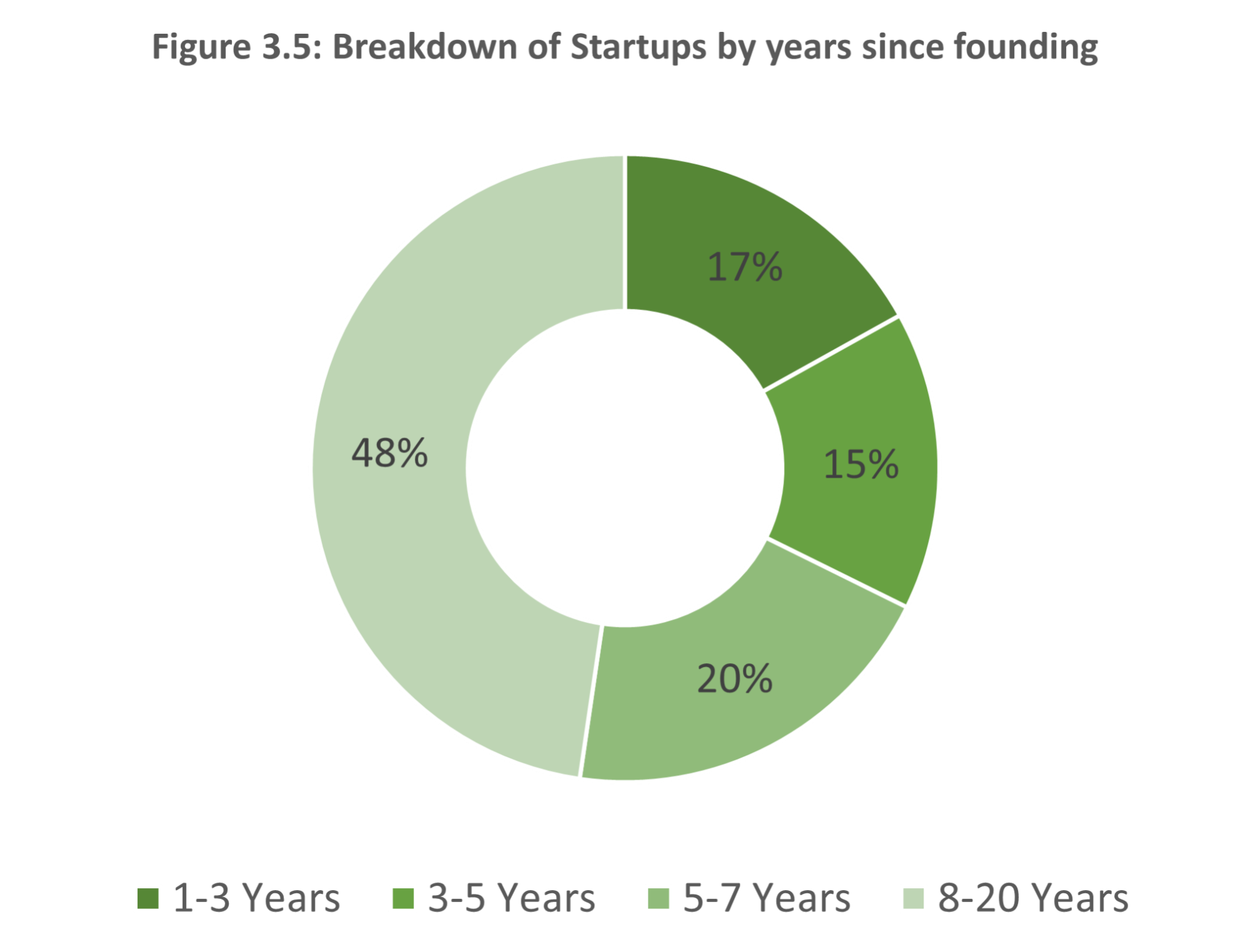

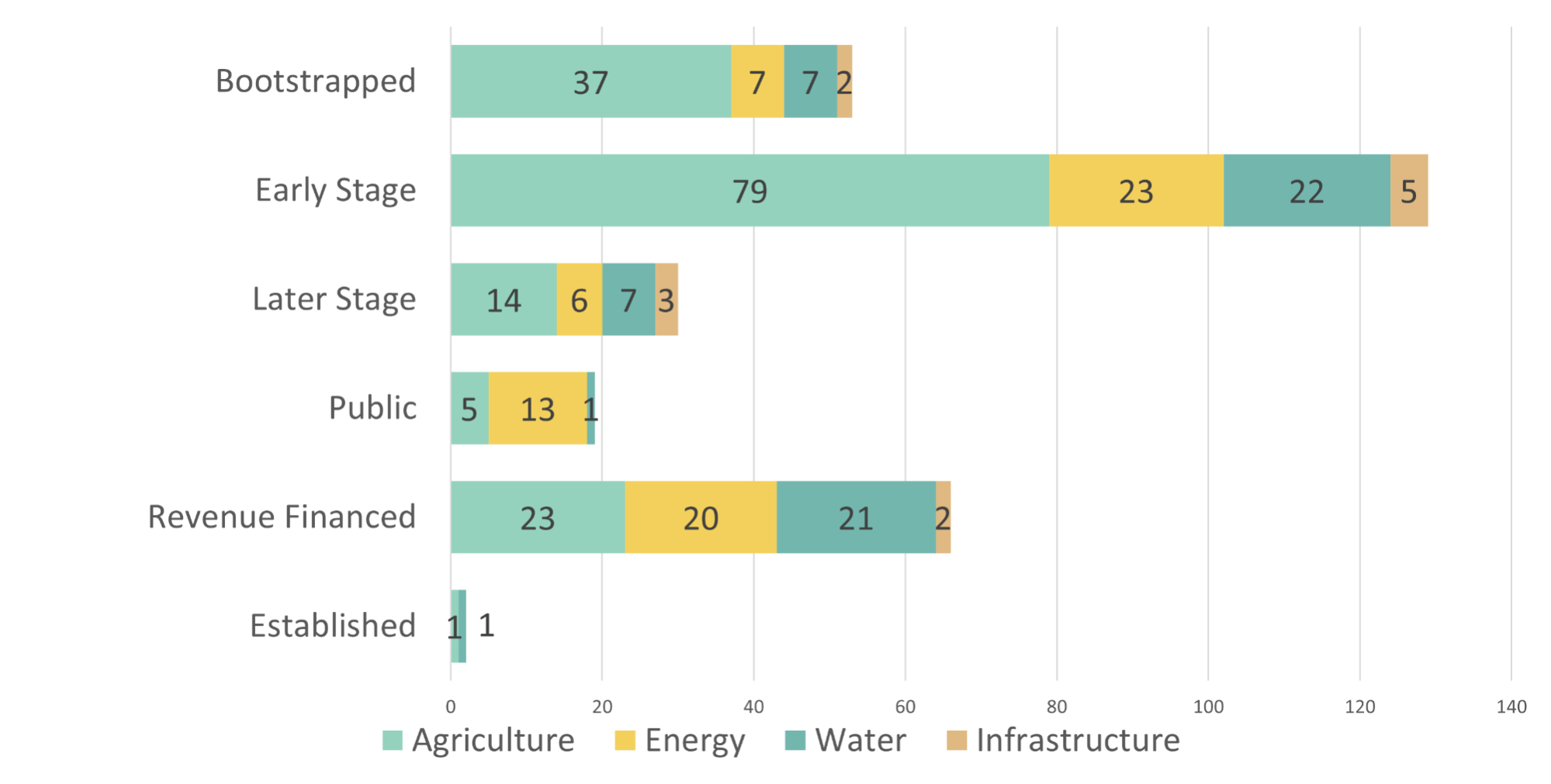

Additional characteristics include the fact that the majority of startups have been in the market for more than five years, with only 32% established in the last five years.

Figure 3.3: Distribution of companies by vertical and stage, number of companies

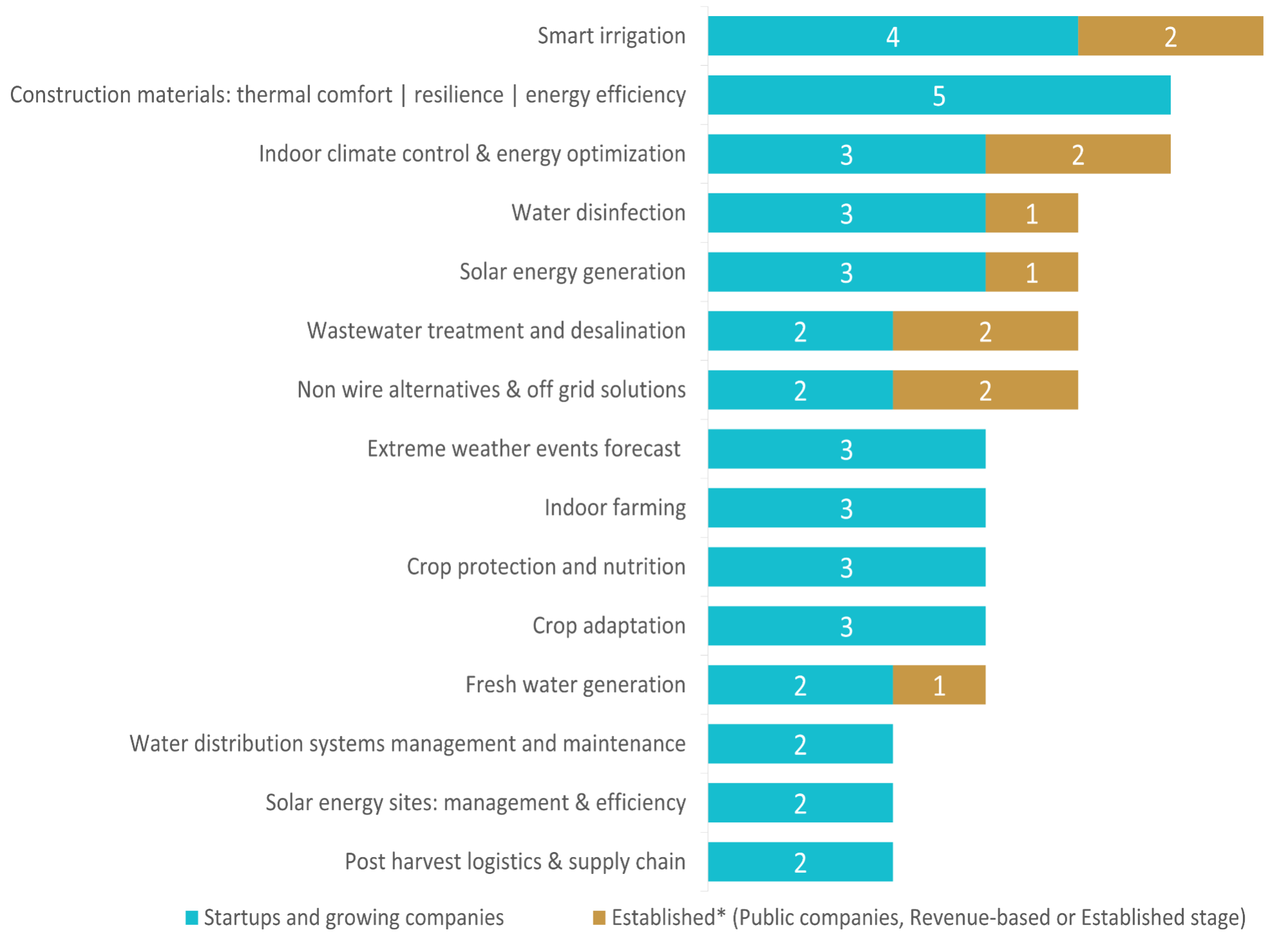

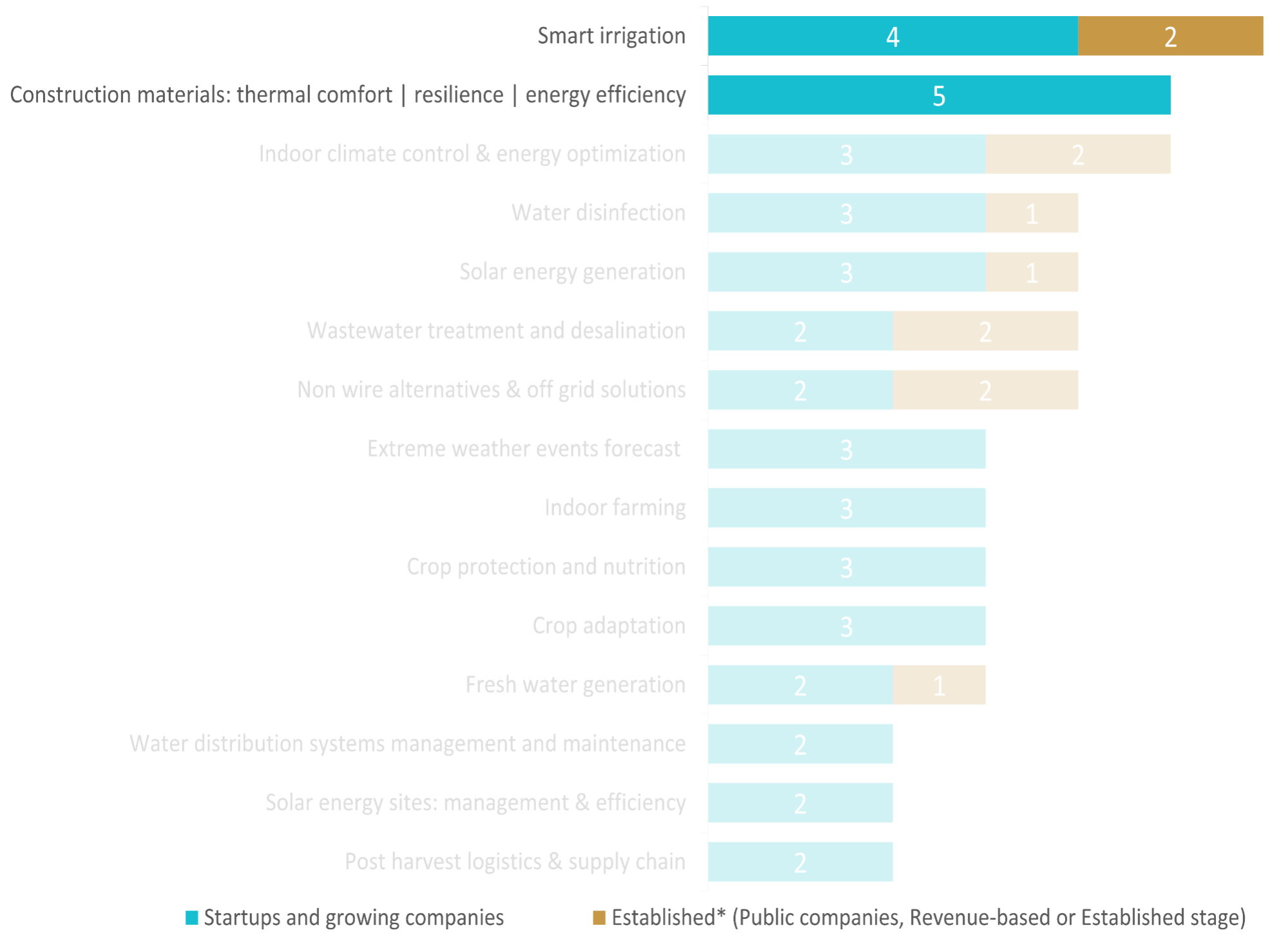

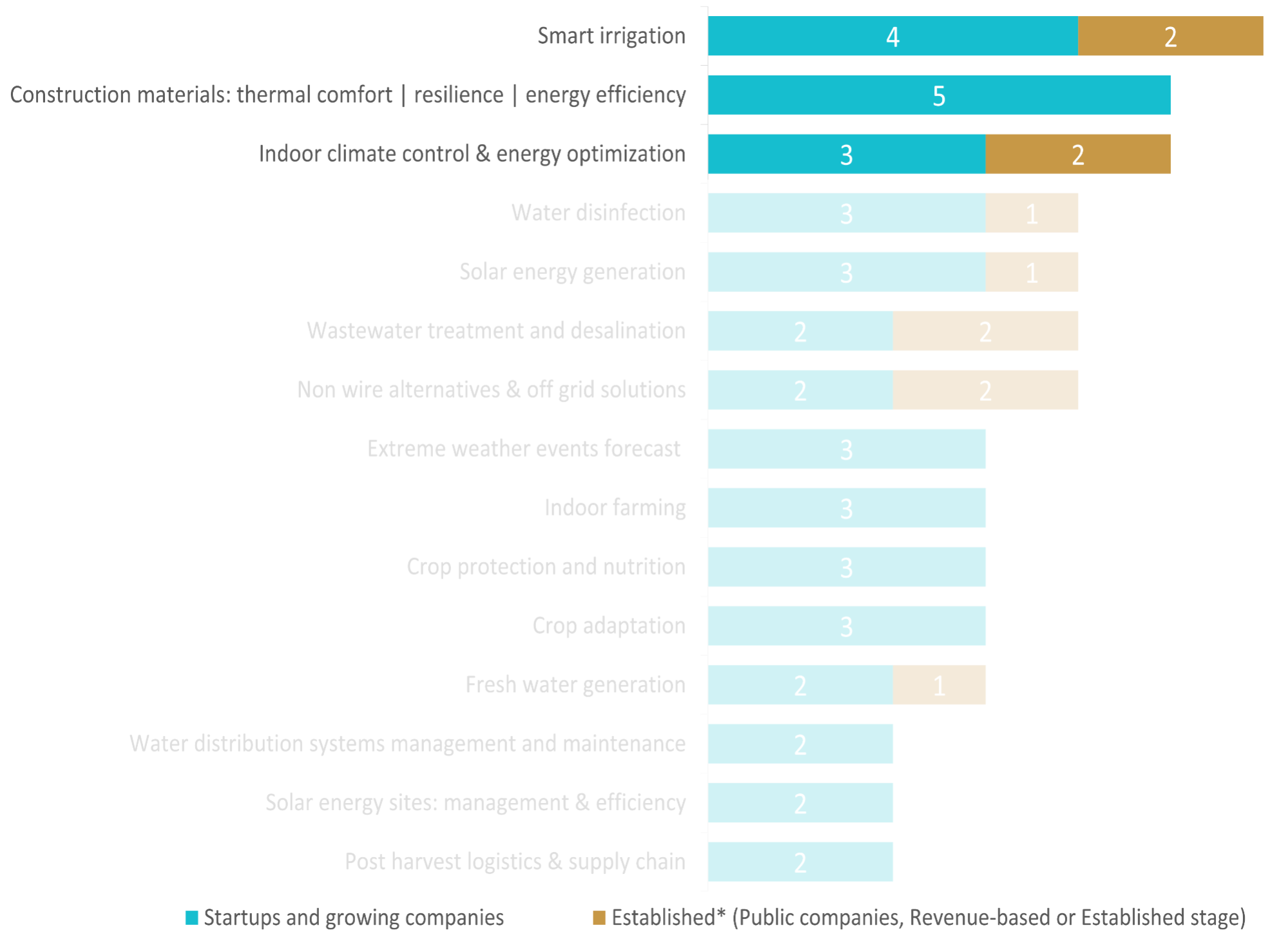

DeserTech startups cover 26 solution fields, seven of which account for approximately 50% of the total number of companies.

These prominent fields are largely focused on water

and energy.

There are also many startups within smart irrigation and construction materials.

These two fields, along with indoor climate control & energy optimization, have raised the most money in their respective verticals, raising between $38M to $89M. Gauzy – a construction materials startup that develops functional glass coatings – raised $60M in a Round D in 2022, and N-Drip – a smart irrigation startup – raised $20M in a Round B in 2021

DeserTech startups cover 26 solution fields, seven of which account for approximately 50% of the total number of companies.

These prominent fields are largely focused on water

and energy.

There are also many startups within smart irrigation and construction materials.

These two fields, along with indoor climate control & energy optimization, have raised the most money in their respective verticals, raising between $38M to $89M. Gauzy – a construction materials startup that develops functional glass coatings – raised $60M in a Round D in 2022, and N-Drip – a smart irrigation startup – raised $20M in a Round B in 2021

Out of the 66 DeserTech companies, 22 have raised a total of $347M. Out of the 4 verticals, agriculture and infrastructure startups together contribute 77% of the total.

Figure 3.7: Breakdown of Total Funding by Vertical (2006-2022)

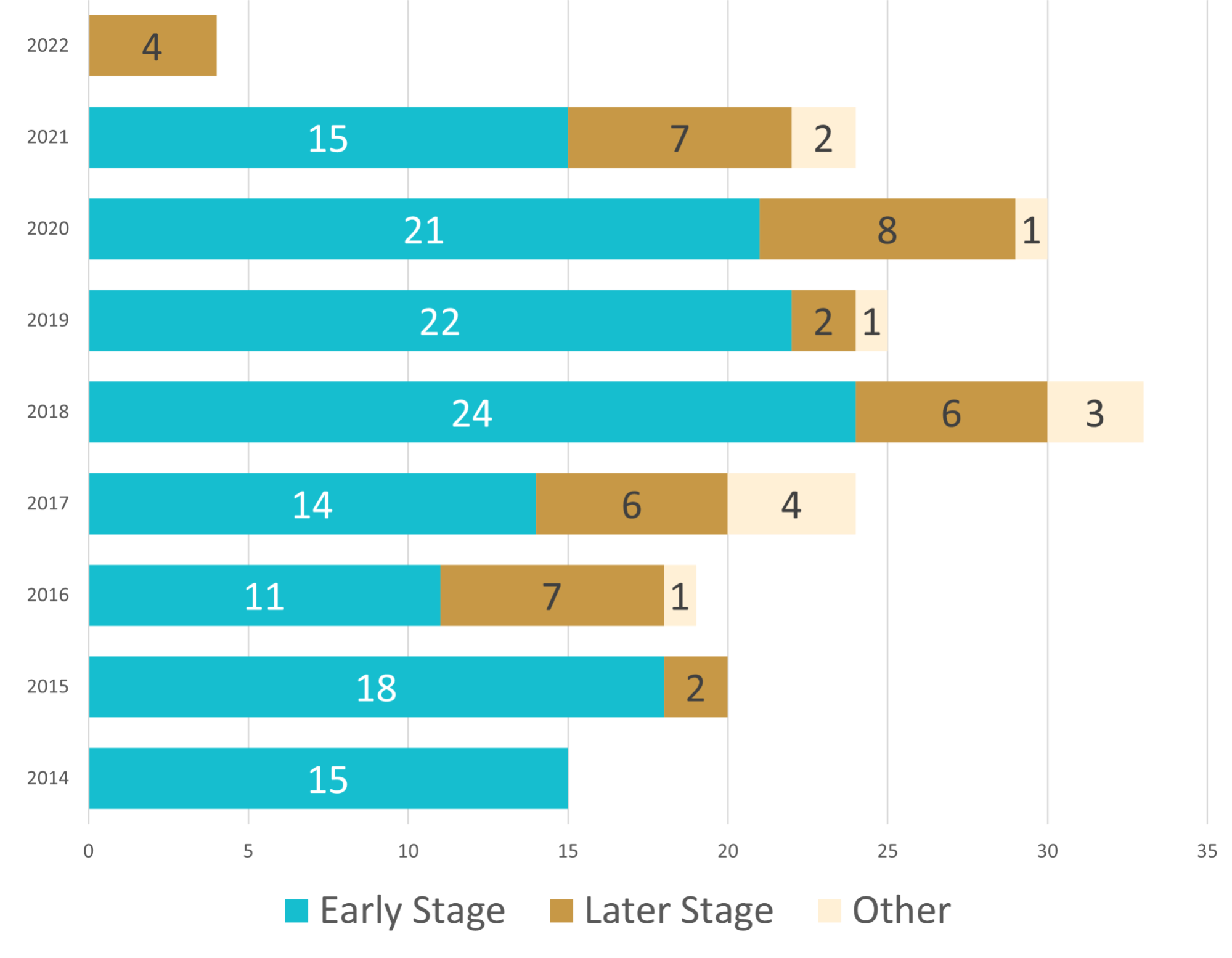

Focusing on the most up-to-date and accurate data from 2014 onward, the median round size by vertical between 2014-2022 was $1.5-4M. Startups from the energy and agriculture verticals were able to close more funding rounds, with 16 rounds and 15 rounds, respectively, raising $122M combined. Startups from the infrastructure vertical, raised $108M in 13 rounds, although it includes only half as many startups as other verticals.

Figure 3.8: Funding raised in each vertical in $M and number of rounds,

2014-2022

$XXM = Median round size in each vertical

Bubble size = Number of funded startups in the vertical

W/O Post-IPO Equity Funding and Debt Financing

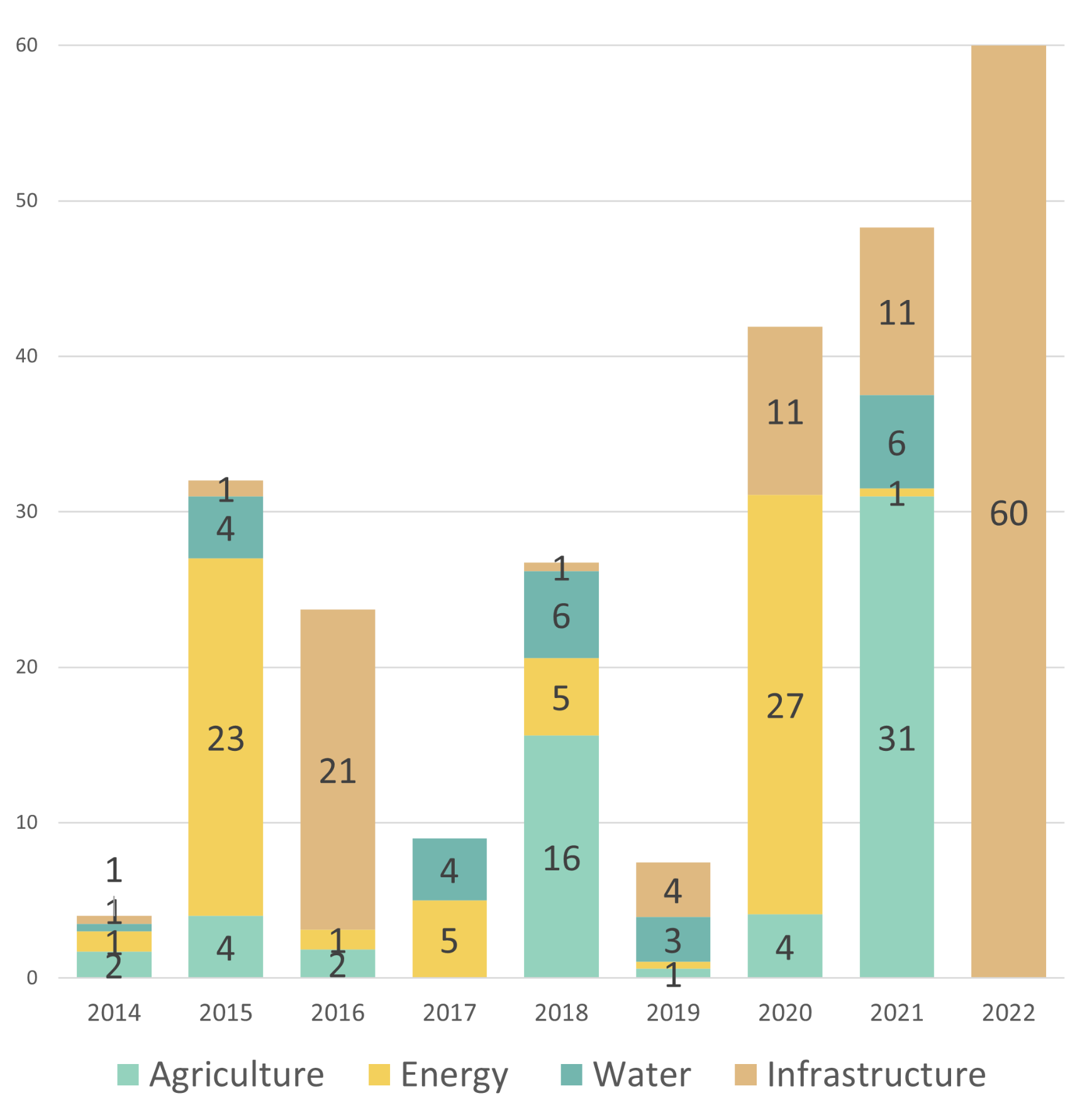

Growing interest in the field can be seen in the steady increase in raised funding since 2017 (except from 2019). From 2017 to 2021, funding raised increased by 437%, a growth rate that is expected to create new emerging fields in areas that are currently in their infancy.

Figure 3.9: Funding raised by vertical, $M

GroundWork BioAg develops and sells mycorrhizal inoculants for commercial farming and raised $11M in 2021 from Israeli and foreign investors. Containing concentrated and vigorous beneficial fungi, the company's Rootella and Dynomyco inoculants can improve soil nutrient uptake in plants, increase crop yields, improve resistance to several types of stress, and reduce fertilizer requirements.

Founded in 2006, Arava Power Company develops, owns, manages, and optimizes utility-scale photovoltaic (PV) systems. In 2011, the company established a commercial solar field in Israel, in Kibbutz Ketura. Throughout the years, the company has established and operates fields with a total output of 120MW.

Founded in 2009, Watergen develops energy-efficient, accessible solutions to generate clean and safe drinking water from the air. It offers 'water-from-air units' in different sizes that can serve a variety of needs and require no infrastructure other than electricity or solar energy.

Kando, a wastewater management solutions company, offers its Kando Pulse digital solution that provides water-quality sensors and samplers, connected to a data fusion and analytics software engine and optimized to deliver operational intelligence in real-time. In 2020, Kando won Seagate's Innovator of the Year competition and in 2021 it raised $6M in a B round – the biggest round within the water vertical that year and the second-biggest round ever within the water vertical.

Gauzy is a functional glass coatings company that develops, manufactures, and markets Light Control Glass (LCG) technology that allows glass to change from transparent to varying degrees of opaque for customized shading, solar control, energy conservation, privacy, and transparent commercial displays. Gauzy raised $60M in a D round in 2022, the biggest round in the vertical.

Asterra, leak prevention solution company, developed satellite-based technology that can identify and locate different types of subsurface water near critical infrastructure such as water and sewer pipes, roadways, and railways. It successfully commercialized its leak-detection product in 2016 and has completed hundreds of projects worldwide. The company raised total funding of $9M.

Since many companies in Israel develop technologies that stem from local conditions, needs, and expertise, it was clear that the potential of the companies that can contribute to dealing with desert challenges is greater than the number of present DeserTech startups. We mapped and identified a significant number of startups that, together with DeserTech startups, compose an ecosystem of 303 startups with the potential to tackle desertification challenges (over the course of this chapter, this potential ecosystem will be referred to as ‘potential DeserTech startups’). More than half of them are related to the agriculture vertical, while energy and water each have 20% of startups, and infrastructure has 5%.

Most DeserTech startups are involved in agriculture.

Figure 4.1: Breakdown of Startups by Vertical

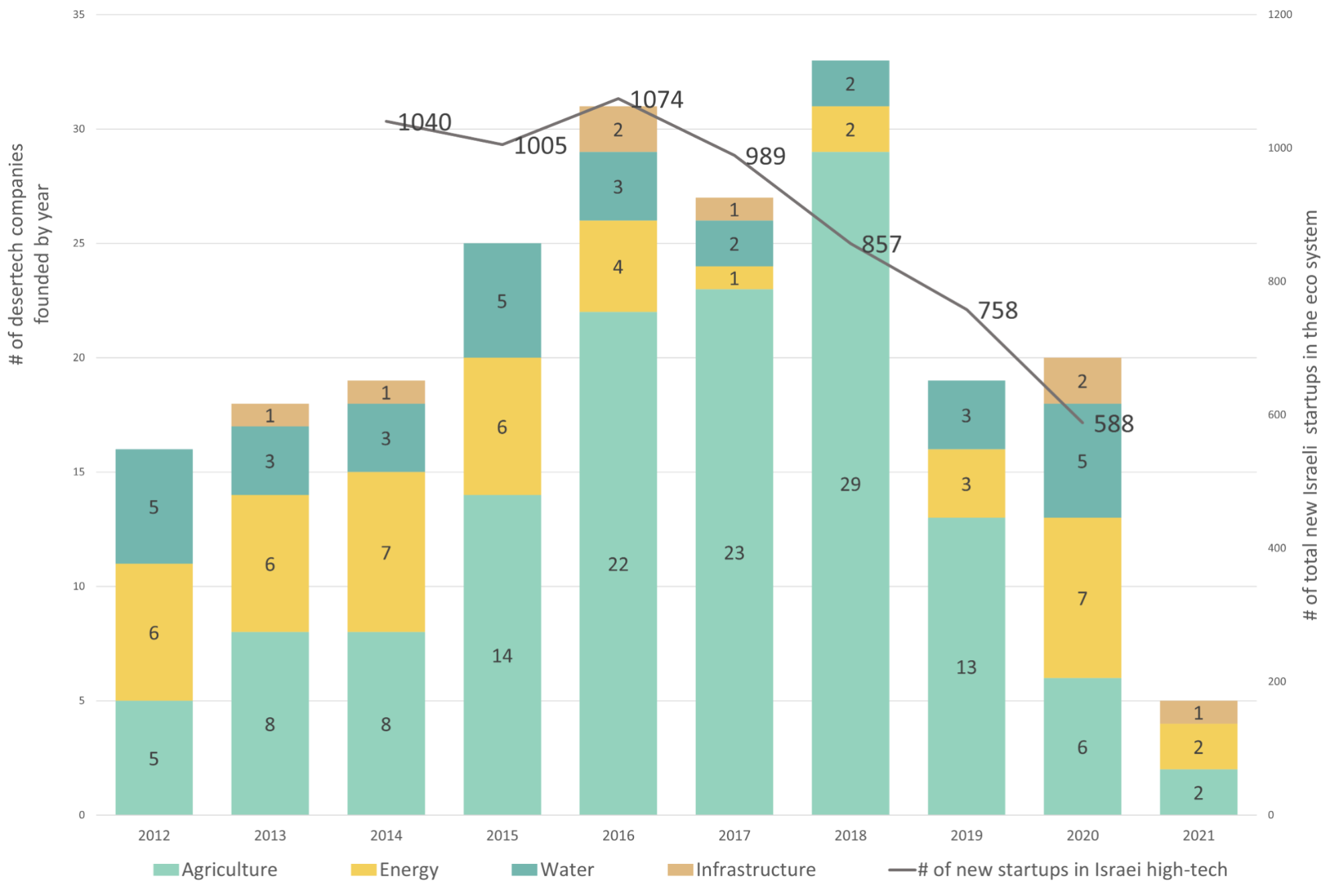

This potential DeserTech startup ecosystem is comprised of relatively young startups – 50% of them being established in just the last 6 years – and it is growing each year, as the number of new companies founded annually increased between 2014 and 2018, remained relatively constant in 2019 and 2020. A positive trend, as opposed to a continuous decline in the number of new startups in the entire Israeli high-tech industry since 2016.

After a steady increase in the number of new startups established each year, this number remains constant in the last couple of years, despite the decline of new startups in the entire Israeli high-tech industry.

Figure 4.2: Number of DeserTech companies founded by year and vertical VS. Number of new startups in the entire Israeli high-tech ecosystem

Similarly to the recognized 66 DeserTech startups, many of the potential DeserTech startups are in their initial stages with 60% of them are in early stages. However, there are differences between verticals; agriculture and infrastructure startups are relatively new, while energy and water are more mature. The agriculture vertical is the least mature, with 72% of startups in initial stages. Additionally, 45% of agriculture startups were founded within the last five years (2017-2021), compared to 22-31% in the other verticals.

Energy and Water are mature verticals

Figure 4.3: Distribution of companies maturity levels by verticals and stage

Agriculture has the highest number of bootstrapped and early-stage startups

Figure 4.4: Distribution of companies by vertical and stage, Number of companies

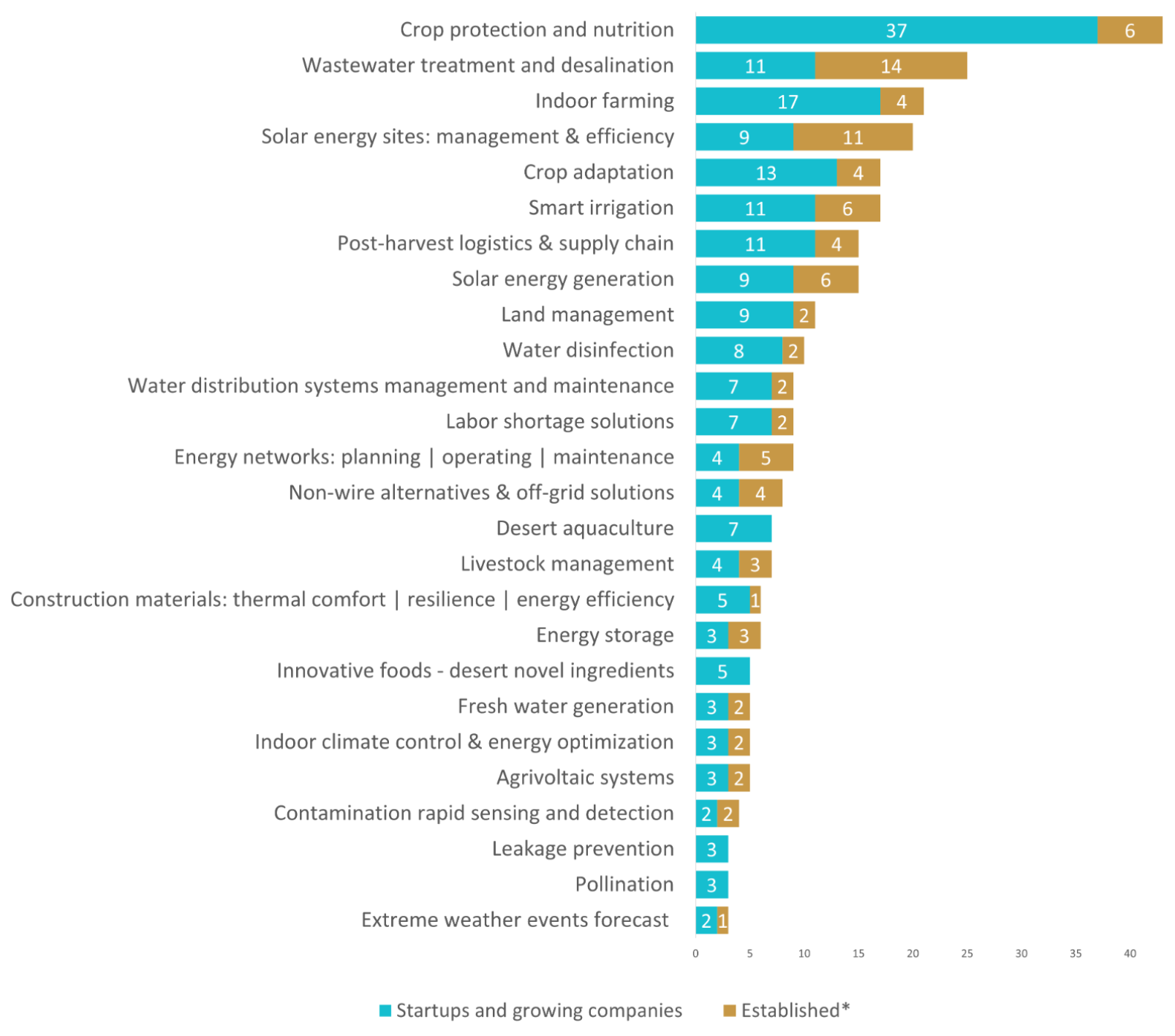

There are 39 different solution areas addressed by potential DeserTech startups, with the most prominent fields being crop protection and nutrition, wastewater treatment and desalination, indoor farming, solar energy sites, crop adaptation, and smart irrigation, together representing 48% of potential DeserTech startups.

Solution areas related to agriculture are the least mature, where 70% of startups are still in the initial stages. In comparison, more mature and established areas like solar energy sites and wastewater treatment & desalination have raised the most or the second-most funding in their verticals. The prominence of these two areas is backed by the fact that Israel is a global leader in water reclamation and recycling; more than 50% of its water comes from recycled or desalinated sources and Israel is the world leader in water reuse. Furthermore, Israel has also been a pioneer in solar energy generation, particularly in desert areas, with the first commercial solar field in Israel constructed in early 2011 in Kibbutz Ketura.

While most of the solutions of the water vertical are mature, there are still many new and promising areas like water disinfection and water distribution system management and maintenance, where 80% and 77% of companies are still in their initial stages, respectively. The latter attracted the largest amount ($27M) within the water vertical, where the most noteworthy round this year was the $15M raised by WINT Water Intelligence, which develops enterprise-grade water management and control solutions.

The overall DeserTech startup ecosystem offers a wide range of solutions

Figure 4.5: Startups by Solution and Stage, Number of Startups

Potential DesertTech startups attracted more than $1.84B in funding from 2006-2022, across more than 272 rounds. Energy and agriculture received 90% of the total funding over this period.

The amount of capital raised by companies increased by 150% between 2019 and 2020, and has remained rather stable, despite stabilization of the number of new companies being created each year since 2019. This paradoxical increase is typically a result of one company raising a large amount of money within its vertical, except in agriculture, where five different companies raised between $20M and $37M each. Furthermore, the agriculture vertical raised $583M from 2014-2022, which is more than all the other verticals combined ($420M in the same period) while demonstrating a trend of steady growth in the amount of money raised each year.

The amount of capital raised by potential DeserTech startups increased by 150% between 2019 and 2020. The agriculture vertical raised more funding than all three other verticals combined.

Figure 4.6: Funding raised by vertical, $M

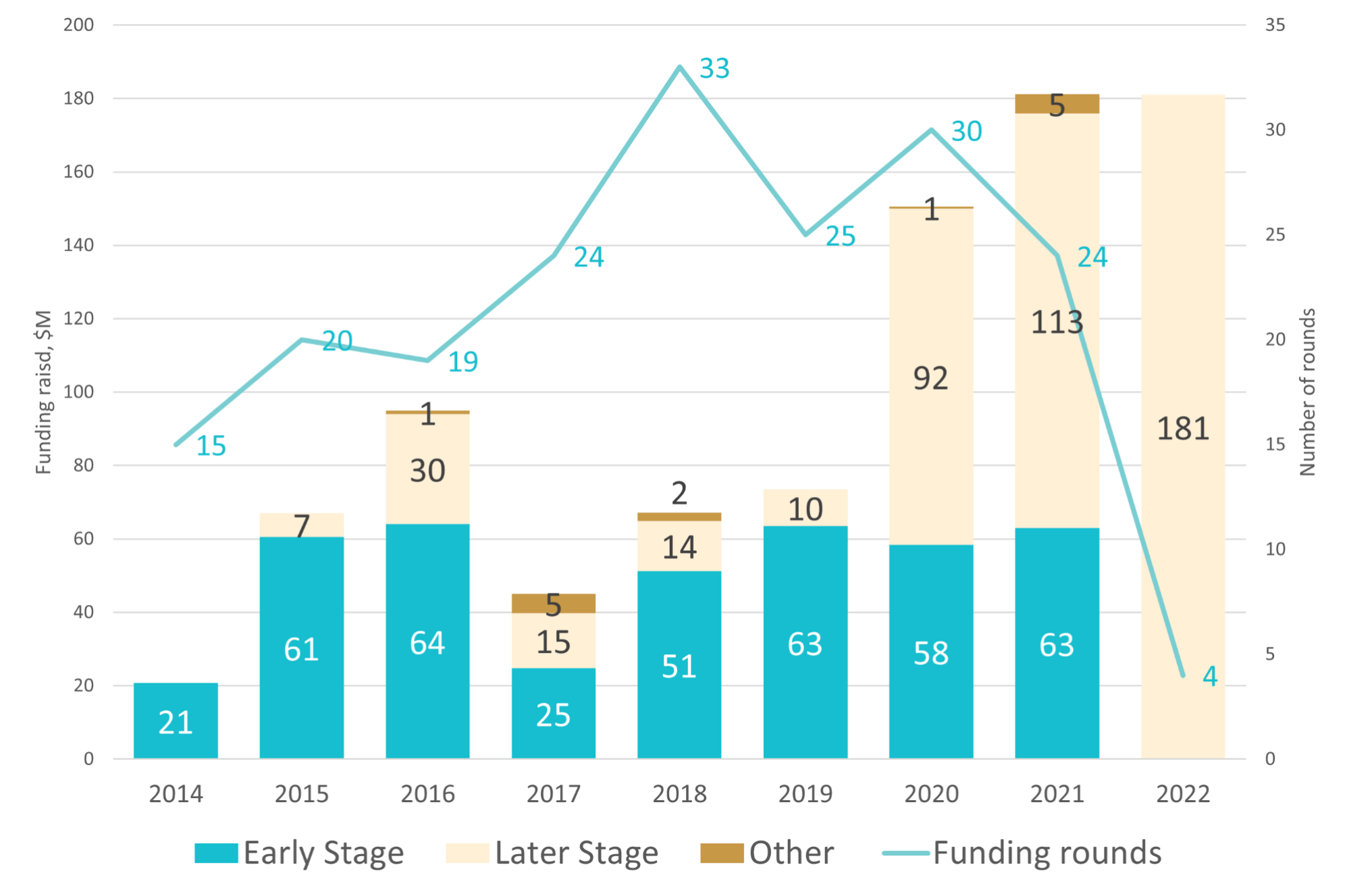

Since 2017, the amount of funding raised has increased, while the number of funding rounds has decreased, pointing to larger funding rounds, on average.

In the last five years, the funding raised grew each year while the number of rounds decreased.

Figure 4.7: Funding raised by round type, $M and Number of rounds

During this time, the number of late-stage rounds has remained relatively constant since 2016 (excluding 2019), while we have seen fewer early-stage rounds since 2018, despite the fact that total funding raised at this stage remained relatively constant. This means fewer early-stage startups raised funds, while more later-stage companies raised higher amounts in their funding rounds, which is typical of more mature ecosystems.

The number of rounds is declining, especially early-stage rounds

Figure 4.8: Number of rounds by stage*

Founded in 2017, SeeTree is an intelligence platform that provides tree-by-tree intelligence to help growers track their health and productivity, and raised $30M in a B round in 2020. With SeeTree, trees and forests can be even more beneficial at stabilizing soil, improving fertility, and protecting against droughts and floods, all of which are crucial to fighting desertification and enabling desert greening visions, such as planting forests in the Sahara, to become a reality

Nostromo Energy has developed the IceBrick ESS, an energy storage system that requires no toxic or rare earth materials. It uses surplus electric power during periods of excess to store cold thermal energy in the form of ice, which is then utilized for cooling during peak hours when the electrical grid is under its highest level of stress. Supported by Shell Ventures, it has raised a total of $7.3M since its establishment

A major enabler and contributor to the initiation and operation of DeserTech startups was and continues to be the Negev Desert. For decades, it has been a living laboratory for developing solutions that will enable sustainable living in an arid climate. Even in the days of David Ben-Gurion, the Negev was declared to be the place where the people of Israel would be examined, and he dreamed that a Hebrew Oxford would be built there - a space of spiritual creation and advanced science.

As early as 1962, Midreshet Sde Boker was established, and scientific desert research institutes were founded to answer basic scientific questions: How can people utilize natural resources like the sun to support themselves and improve their quality of life? How can they overcome natural challenges such as extreme water scarcity?

At the same time, throughout the Negev, more communities arose and had to deal with the extreme climate, the low accessibility to infrastructure, and the scarcity of the necessary resources. Additionally, large industrial plants were established in the Negev, relying on the natural resources unique to the region.

Today, there are dozens of basic and applied research institutions in the Negev. They are leading not only in the development of solutions for the farmers who provide agricultural produce to the entire country, but also in the research using existing resources to improve the lives of residents of the Israeli deserts and around the world. These institutions include Ben Gurion University (with branches in both Midreshet Sde Boker and Eilat), Sami Shamoon College, the Gilat Branch of the Volcani Institute, Sapir College, and the Arava Institute, as well as agricultural and scientific R&D centers Ramat Hanegev and Central Arava, among others. Alongside them, we can find large industrial facilities in the fields of chemistry, pharma, and agriculture, such as ICL, Adama, Teva, and SodaStream.

The diversity of the communities in the Negev also enables the development of many technological solutions that address the needs of life in it. For kibbutzim and moshavim that mainly rely on agriculture for income, we have seen the establishment of various industry associations that promote regional economic development and address the need to improve the quality of life in arid environments. Some factories include Netafim in Kibbutz Hatzerim, Aquasitia-Dorot in Kibbutz Dorot, Ardom in the Eilot Regional Council, Negev Ecology in Kibbutz Mishmar Hanegev, Avshalom in the Eshkol Regional Council, and more.

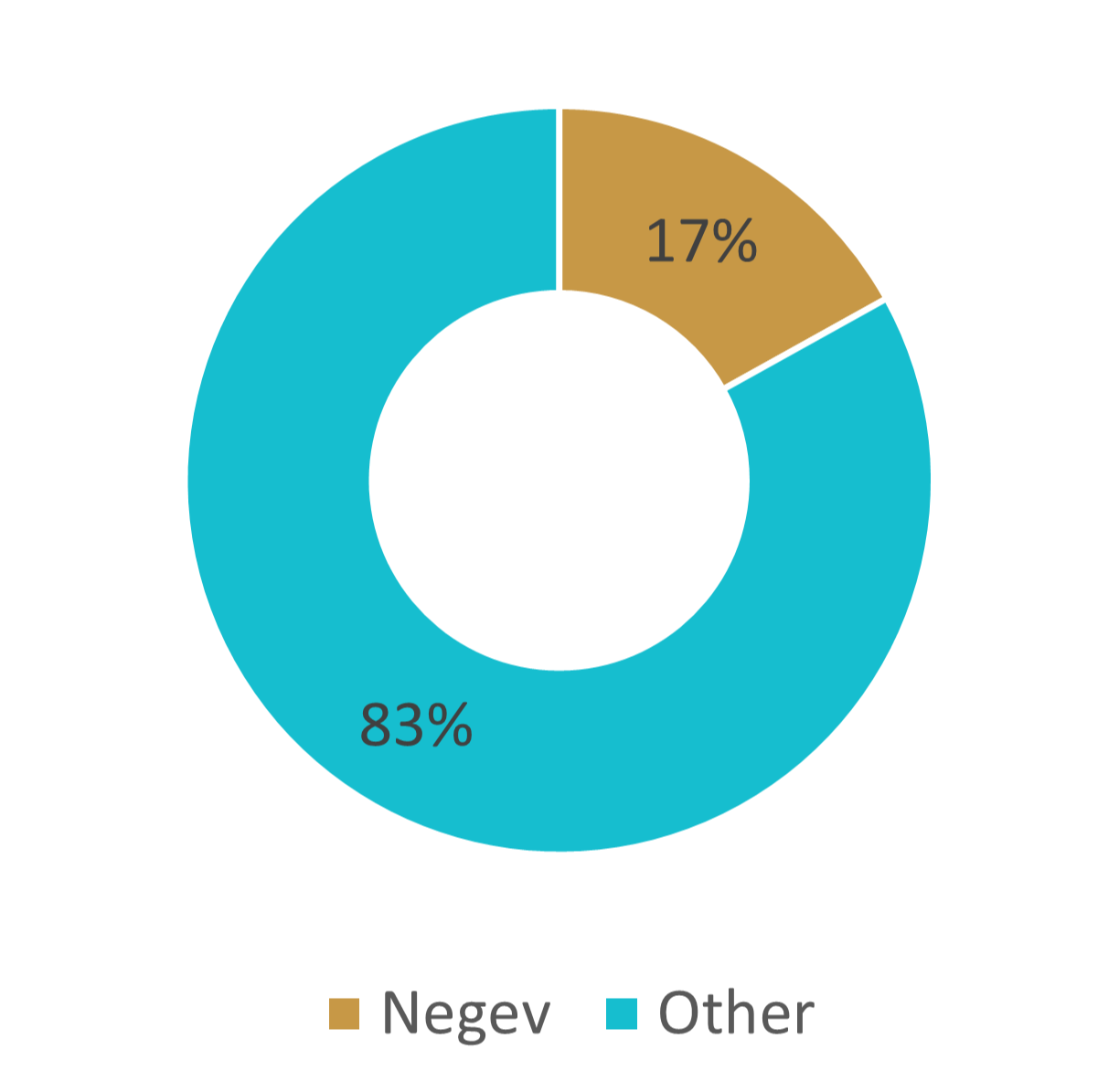

These enabling factors contributed to the fact that today about 17% of DeserTech startups are from the Negev, which is much higher than the share of all Israeli startups in the Negev - 2-3%. In the last few years, there have been several new initiatives aimed at developing startups and new industries in the Negev. This is in accordance with the fact that over 80% of the DeserTech startups in the Negev are bootstrapped or in early stage, while 70% of them are in the agriculture and energy verticals.

Figure 4.11: Breakdown of DeserTech Israeli companies by location