2022:

Two distinct periods

Israeli high-tech industry’s business variables returned to their long-term averages.

The year should be seen as two distinct periods representing roughly the two halves of the year.

Writers: Eran Igelnik, Assaf Patir, Sharon Kinory, Angelina Usim

Design: Hadas Shezaf

In 2022, Israeli high-tech industry’s business variables returned to their long-term averages,

comparing to 2021

VC investments

The second highest year after 2021

Deals

Similar to the multi-year average

M&As (First time exits)

A slight decline in the multi-year trend

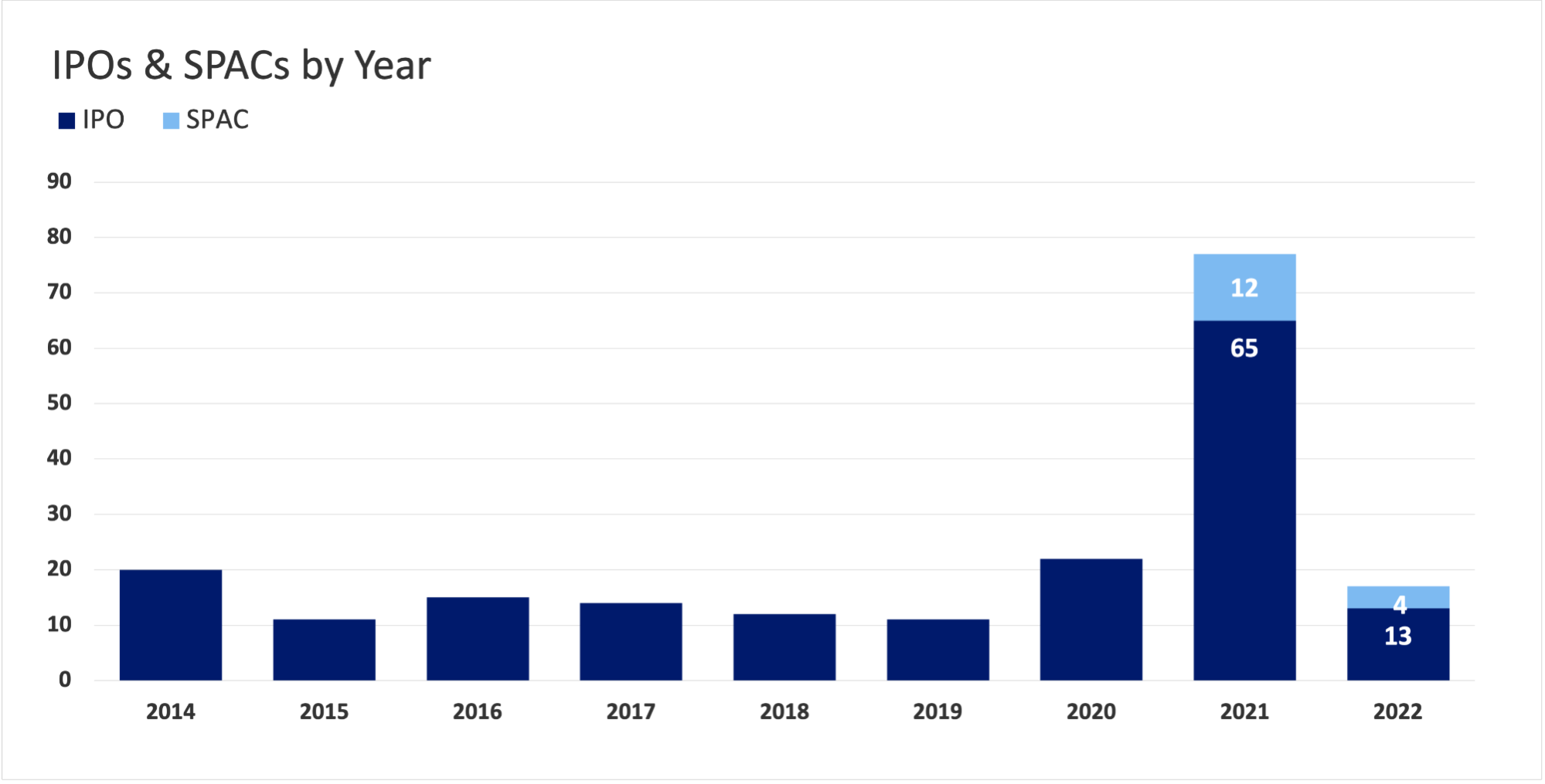

IPOs & SPACs

A return to the range of previous years (10–20)

Israeli high-tech industry’s business variables returned to their long-term averages.

The year should be seen as two distinct periods representing roughly the two halves of the year.

was a continuation of the record-breaking 2021, with extremely high levels of capital funding, soaring market capitalization (market cap), and high demand for workers resulting in rising wages.variables returned to their long-term averages.

was already characterized by the decline in the financial markets and fear of a deep global recession. During this half, we witnessed a decline in the number of deals and their overall value, a low number of exits, a sharp decline in the value of publicly traded tech companies, and an almost complete halt in the “employees’ market” phenomenon.

On the surface, there is a clear connection between these developments, as the global slowdown had a direct impact on both companies’ market value and on their readiness to invest in Israeli high-tech.

However, in this report we offer an additional explanation for the decline in activity during the second half of 2022. Based on a statistical model used to examine the time between investment rounds (between seed and A, A and B, etc.), we found that in some of the cases, the ostensible declines are better described as funding rounds that simply occurred earlier than anticipated, and not decreases in the amount of capital raised. Companies that, according to past data, were expected to raise capital during the second half of 2022, took advantage of the favorable conditions of 2021 and early 2022 to raise money earlier than expected.

At the other end, our model suggests that many investors seeking to invest in A rounds, for example, during the second half of 2022 found that the supply of companies looking for such investment was relatively limited. It is possible that some of these investors chose instead to invest in seed rounds, given that these were the only investment round in which we have seen an increase in investments in 2022 – a phenomenon that can also be explained by the shift of investors from late stage to seed funding and by a sharp increase in the average number of investors in each seed round.

This is not to say that the emerging global recession did not have an impact on Israeli high-tech in 2022 – it certainly did. The declines in market cap can clearly be attributed to the rising interest rates of central banks and the expectations of a recession, while the extensive layoffs and widespread freeze on employee recruitment were the result of the emerging consensus that the “party” is, at least for now, over. However, in this report we offer a supplementary explanation that in addition to being caused by a global macroeconomic shock, the second half of 2022 downturn was also the result of a natural decline caused by two years of abnormally high investment activity.

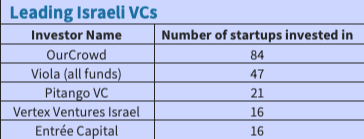

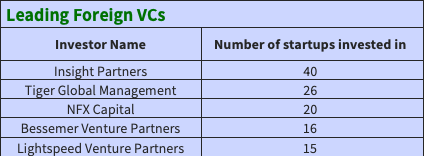

The leading investors were OurCrowd, Viola (all funds) and Insight Partners. Each one of them invested in over 40 different startups during 2022.

The leading sectors in terms of investment were software based, primarily Enterprise Software, Security Tech (which includes Cyber) and FinTech.

Only in Agri & Food Tech we see stability in both number of deals and in their total amount, compared to 2021.

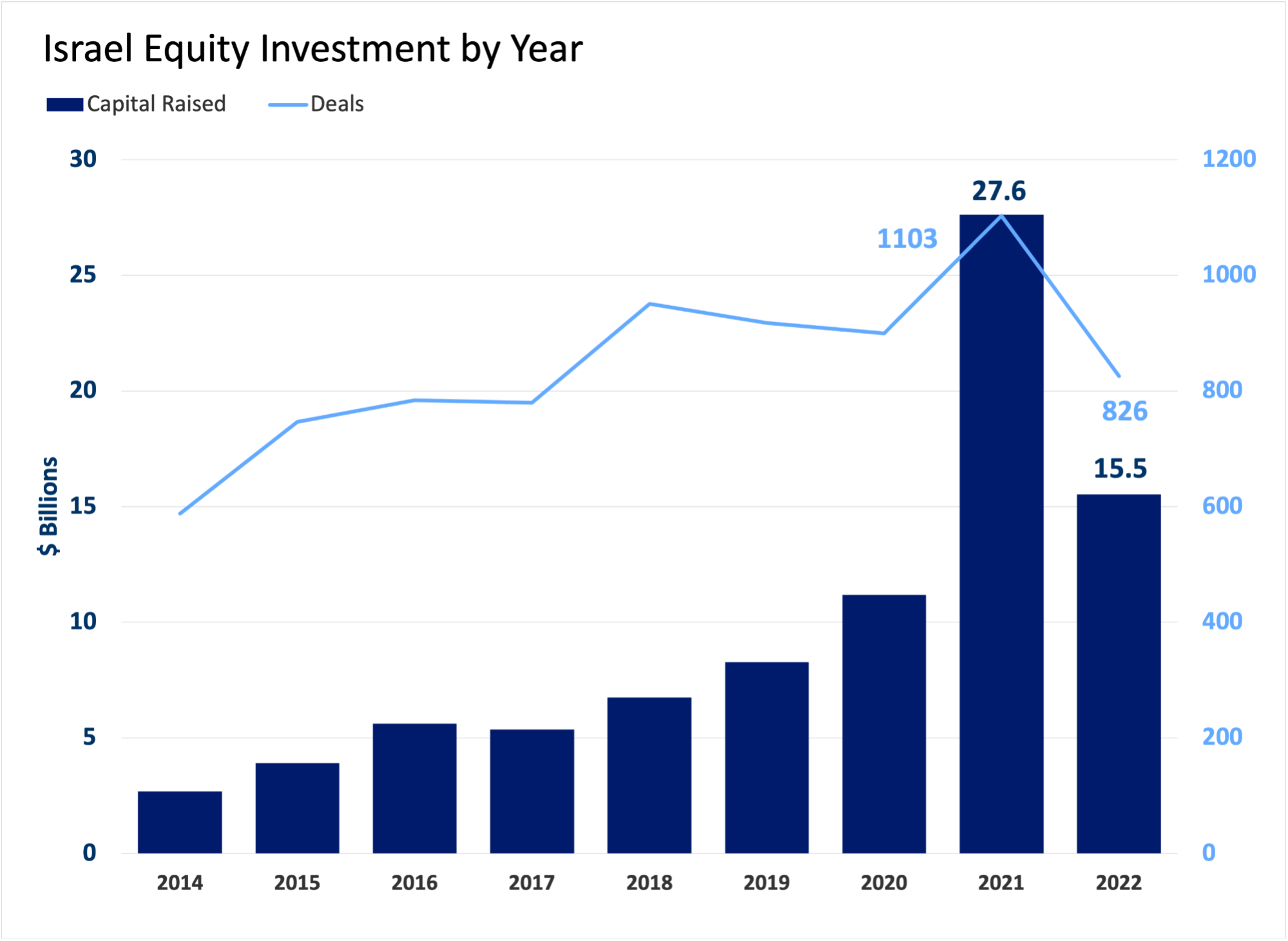

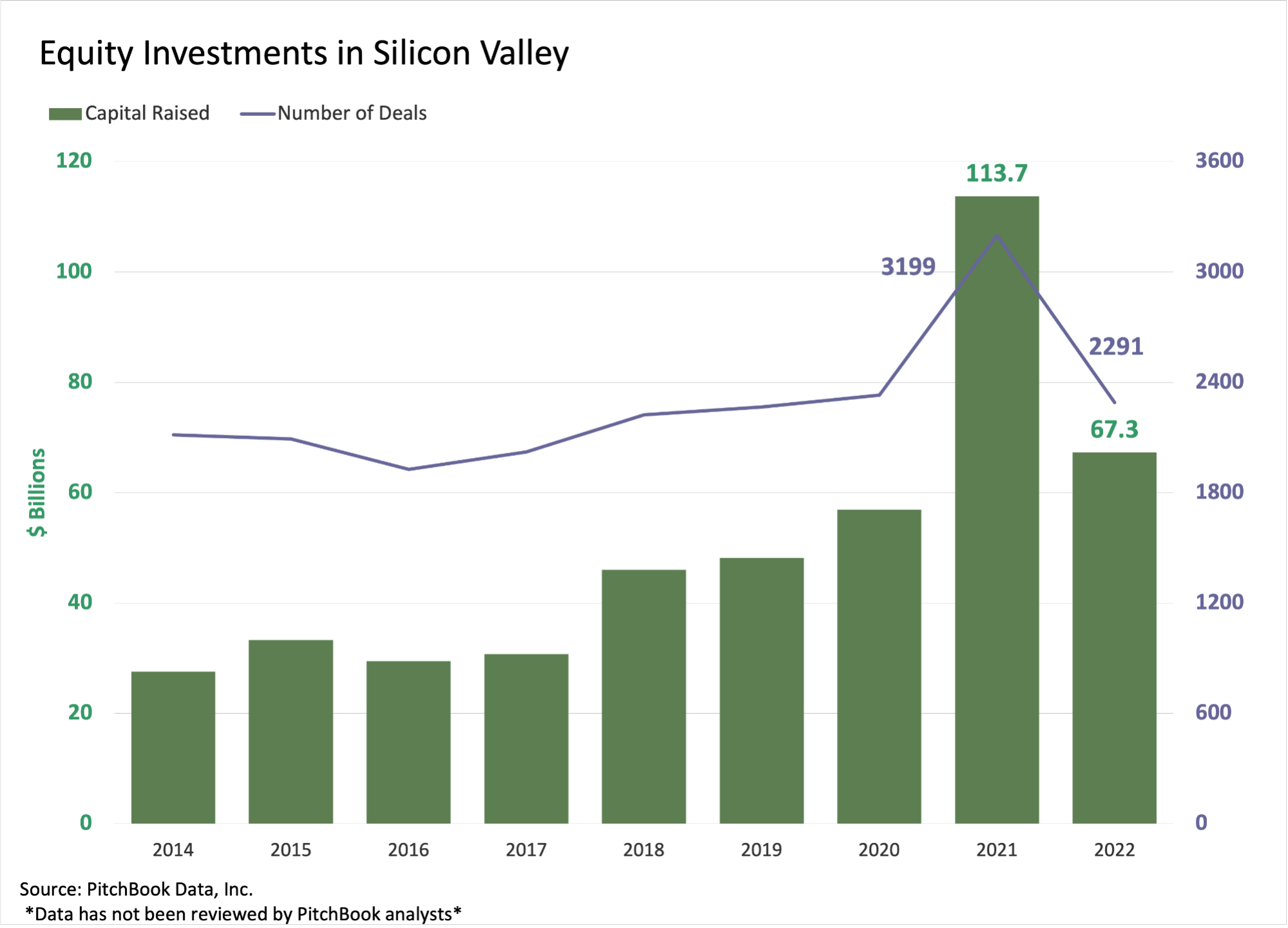

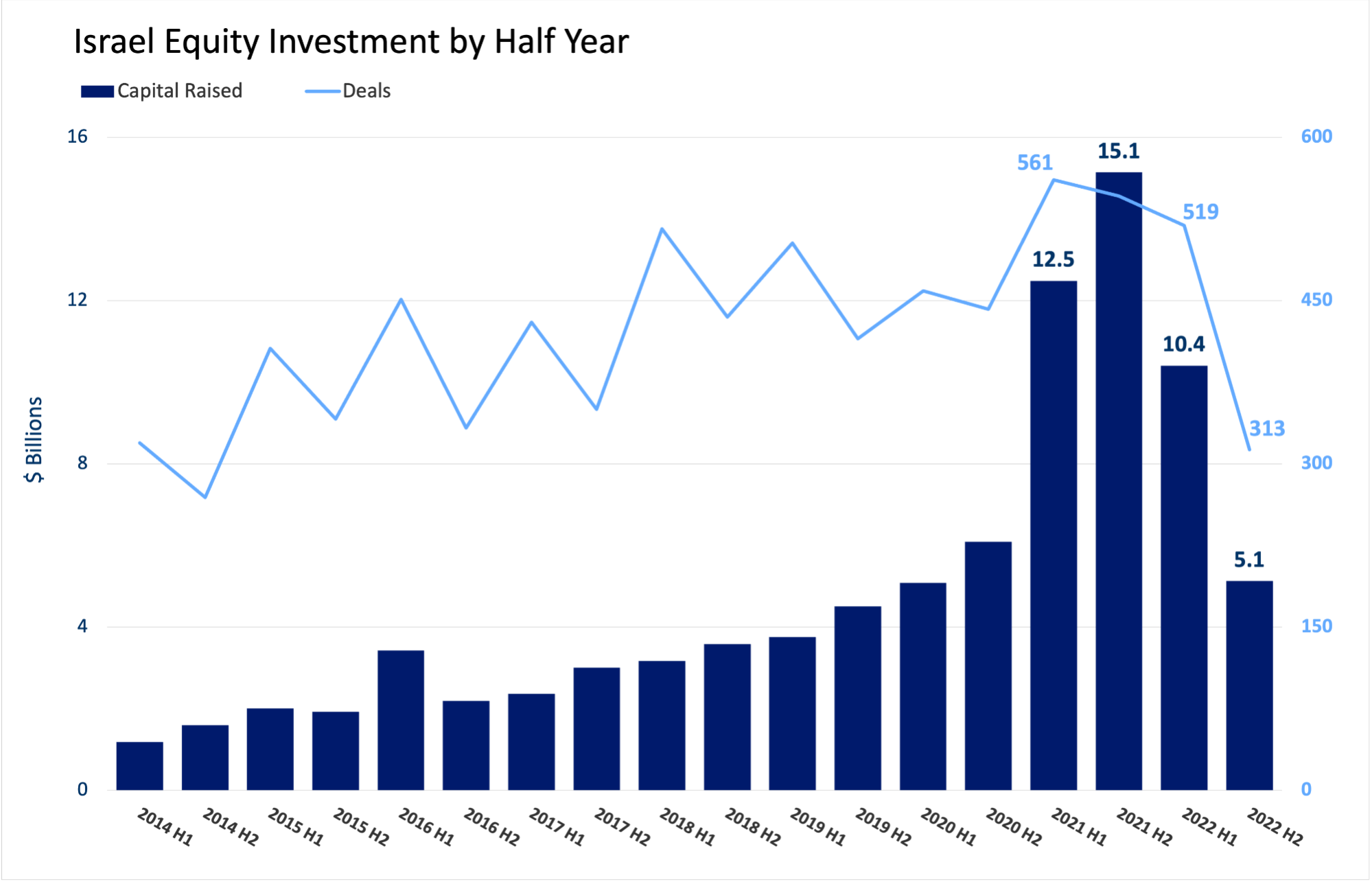

2021 was an exceptional one in terms of the global technology sector’s activity, and Israel was no different, with an unprecedented USD 27 billion invested in Israeli tech companies. In 2022, the volume of investments plummeted by almost half to some USD 15.5 billion.

This phenomenon is not unique to Israel. In Silicon Valley, investments in high-tech companies declined by 40%. The number of rounds declined accordingly by about one third, both in Israel and in Silicon Valley, so that the overall number of rounds in Israel in 2022 amounted to 826 compared to 1,103 in the previous year.

By looking at the data fin six-month increment one can see the initial signs of the slowdown. The first half of 2022 was a direct continuation of 2021, during which USD 10.4 billion were raised, representing two thirds of the total capital raised throughout the entire year.

Although this figure is 31% lower in comparison with the second half of 2021, the 519 deals indicate that the Israeli high-tech industry was still in a boom period. However, during the second half of 2022, there were only 313 deals, the second lowest figure on record. Despite these declines, the amount of investment in the second half of the year was still the largest in recent years, apart from the four half-years preceding it.

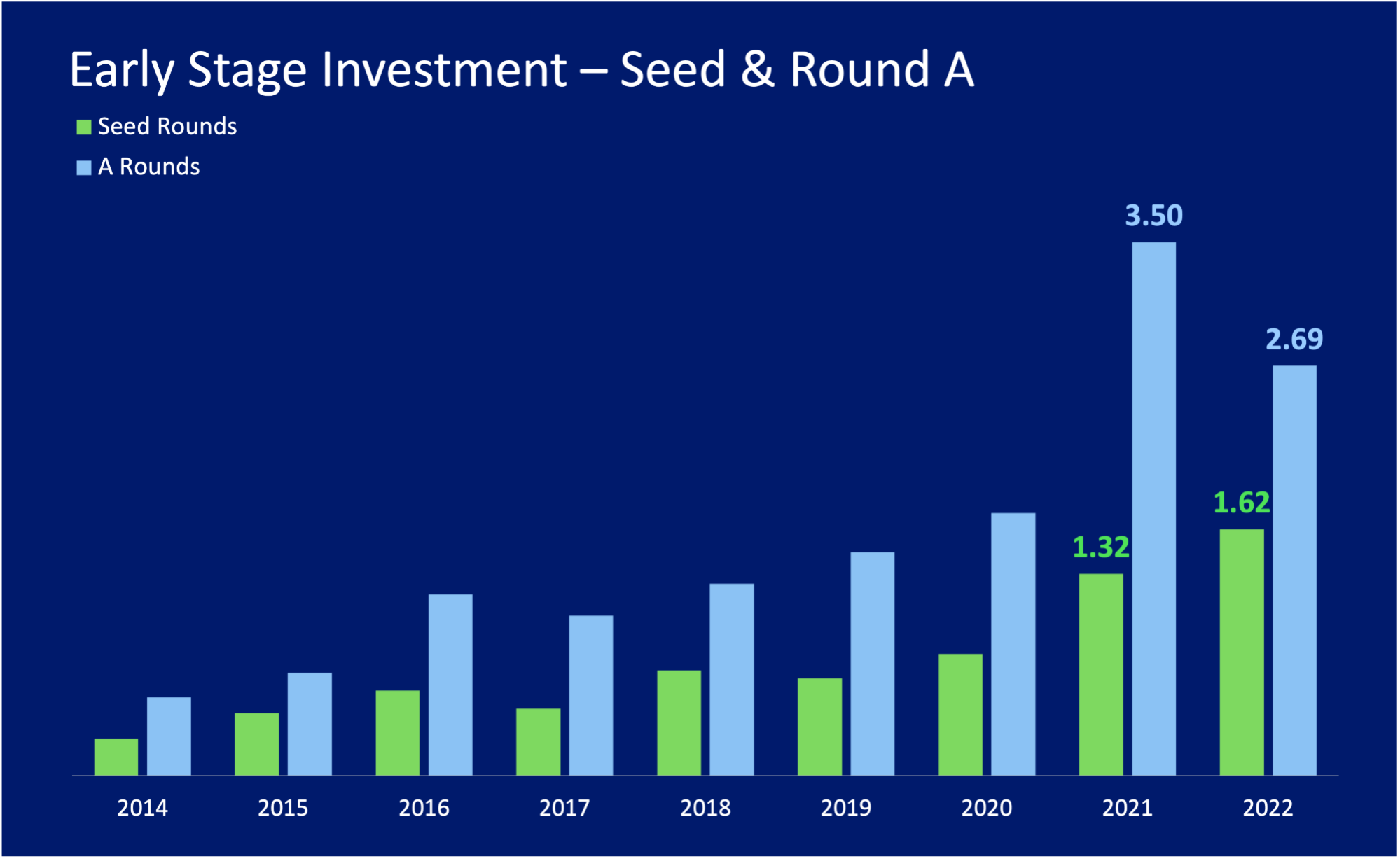

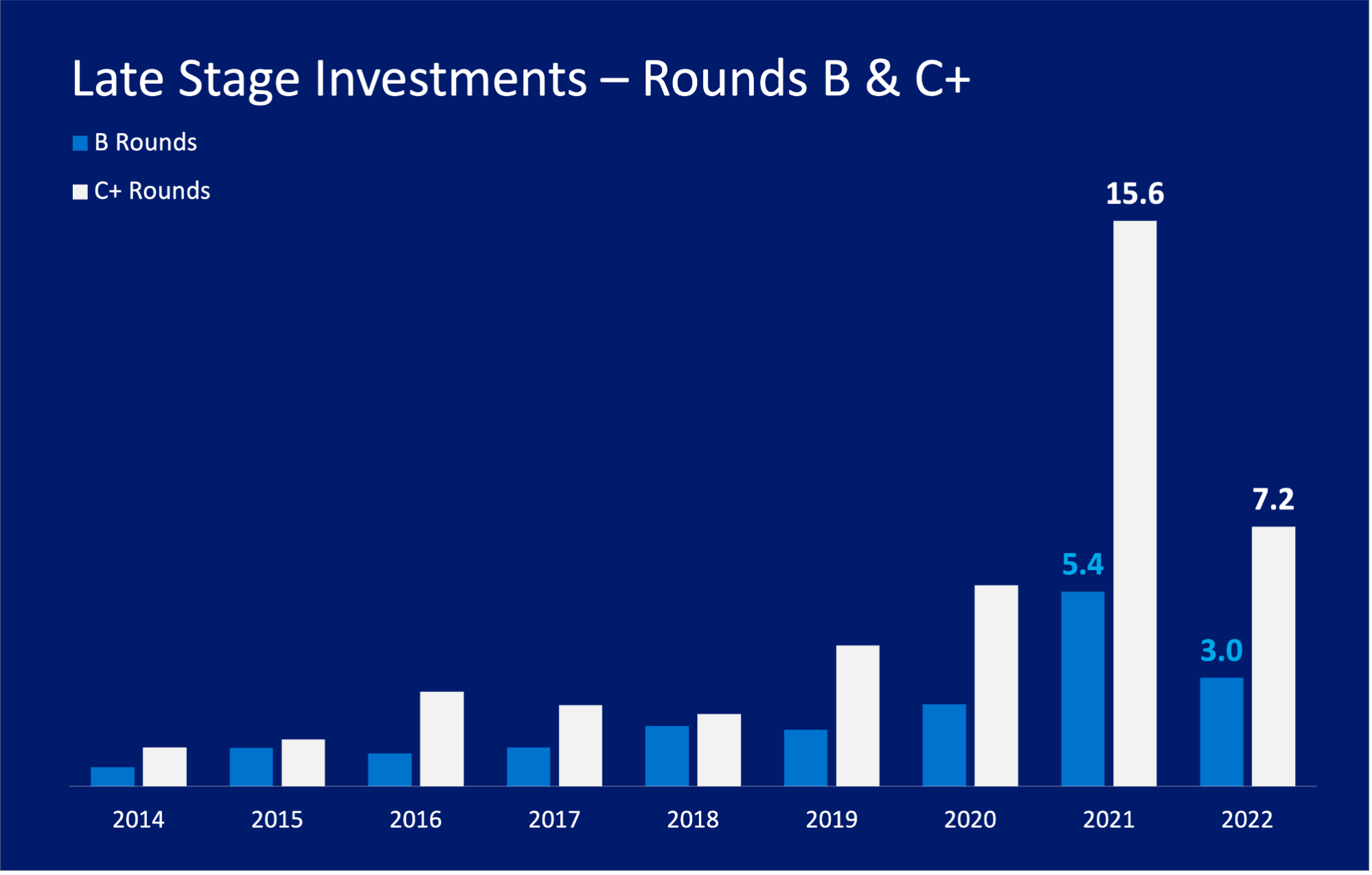

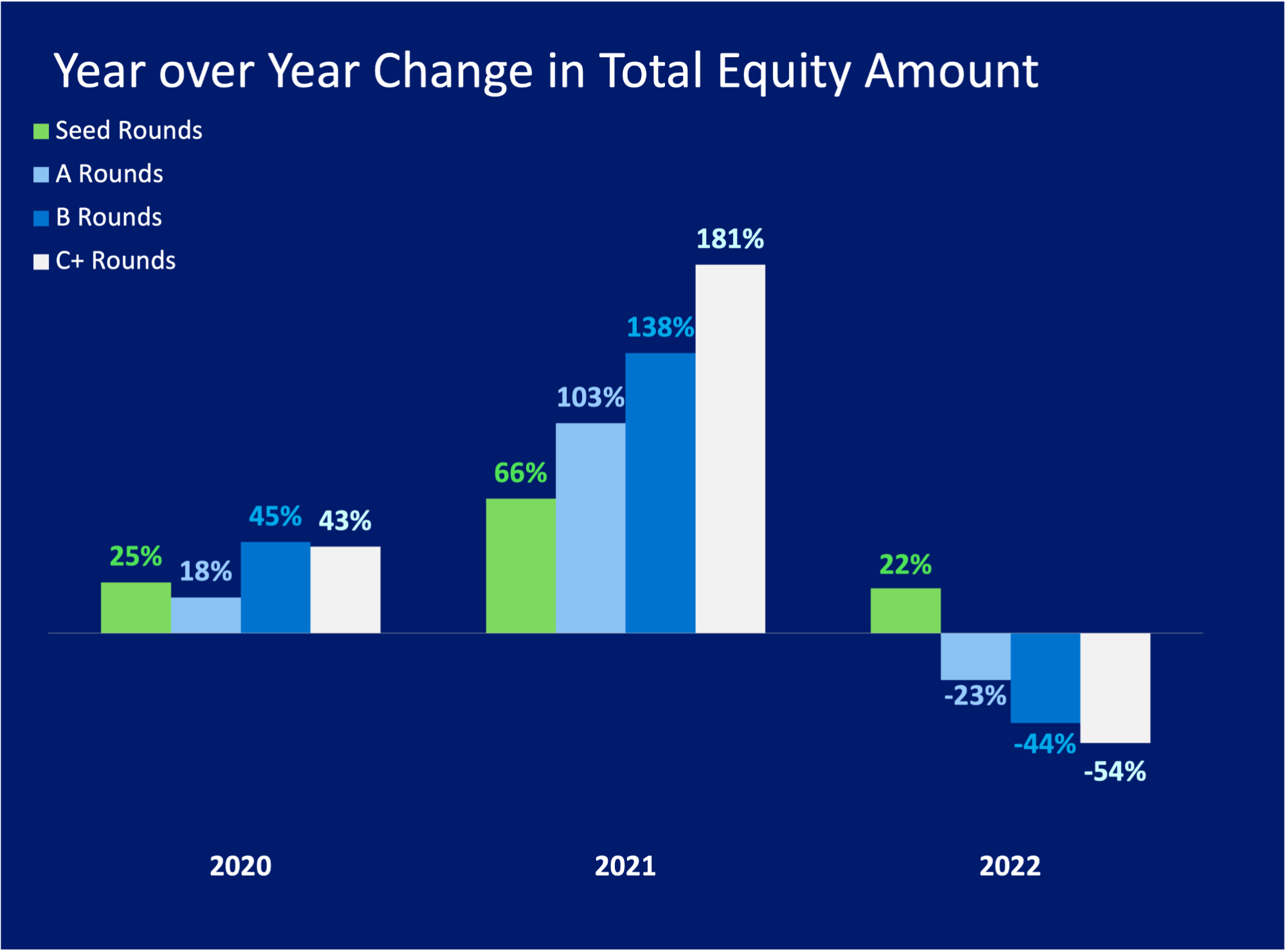

Considering the downturn in the financial markets in 2022, it is not surprising we saw a decline in total investments in most types of investment rounds. Notably, however, seed investments increased in 2022. The Graphs below show the absolute amounts of investment, with a breakdown according to investment years, and the annual percentage change, broken down by investment rounds.

Seed investments in Israeli startups grew by 22% in 2022 compared to 2021, from USD 1.3 billion to 1.6 billion (this figure is expected to further rise due to the time lag in receiving data for deals that have yet to be published). These figures are especially surprising when we take into account the decrease in the number of startups (which we previously reported) which one would have assumed, would lead to a decline in the overall amount of investment in seed rounds.

The data suggest two factors are contributing to the rise in seed rounds:

Some of the increase in seed investments is a result of a shift to earlier stage investments by investors who had traditionally invested only in later stages. According to our analysis of all the investors in the Israeli high-tech industry since 2014, 17 different investors, who until 2021 had invested only in A rounds and above, participated in 22 seed rounds during 2022. While there are several reasons for prioritizing seed investments over later stage rounds, the main reason appears to be the extremely high valuations in the later stage rounds. To illustrate, by the end of 2021, the large investment firm, Tiger Global, had participated in 23 late-stage investments and only one seed investment in 2021. By comparison, in 2022 alone, Tiger Global participated in three seed investments in Israel, with an average value of USD 50 million.

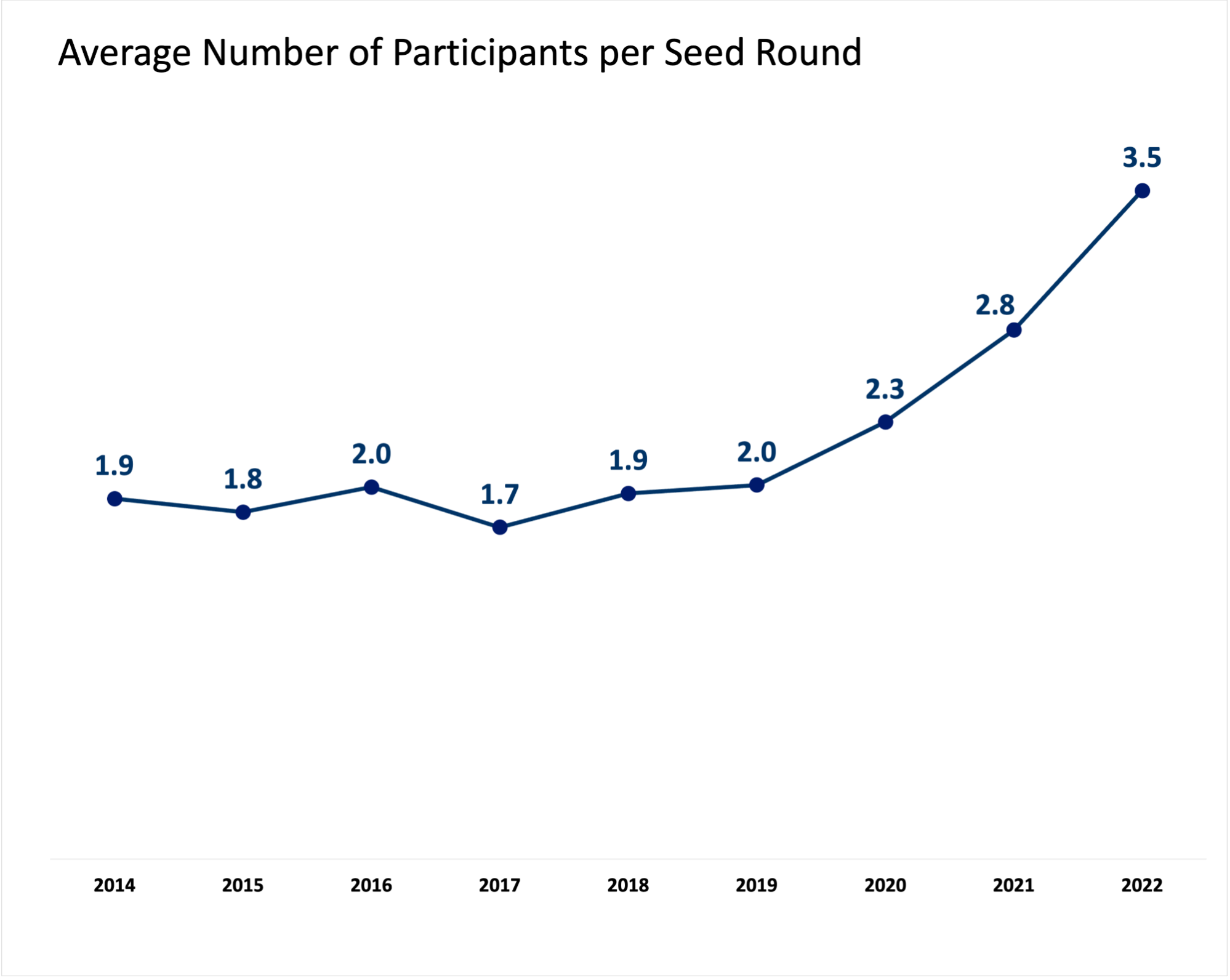

The average number of investors in each early-stage round is on the rise, and this trend is especially prominent in the seed rounds. Between 2019 and 2022, the average number of investors in each seed round nearly doubled. The most significant increase occurred in 2022, when an average of one additional investor was added to each round compared to the 2021 average.

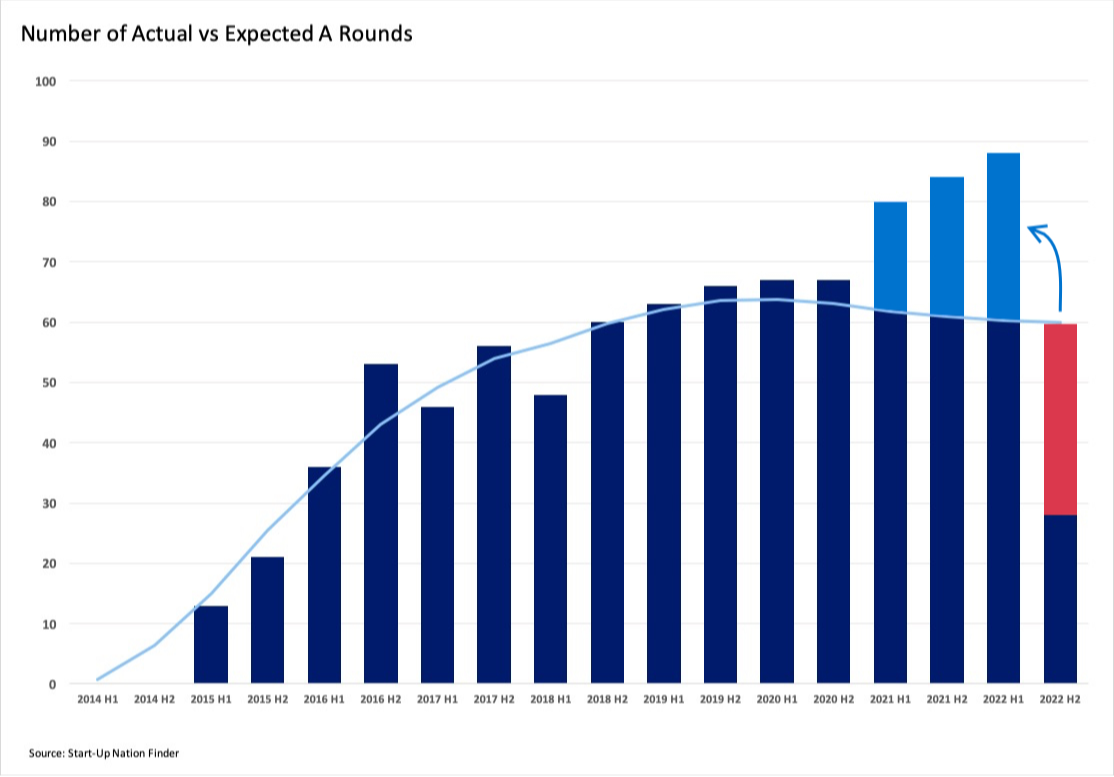

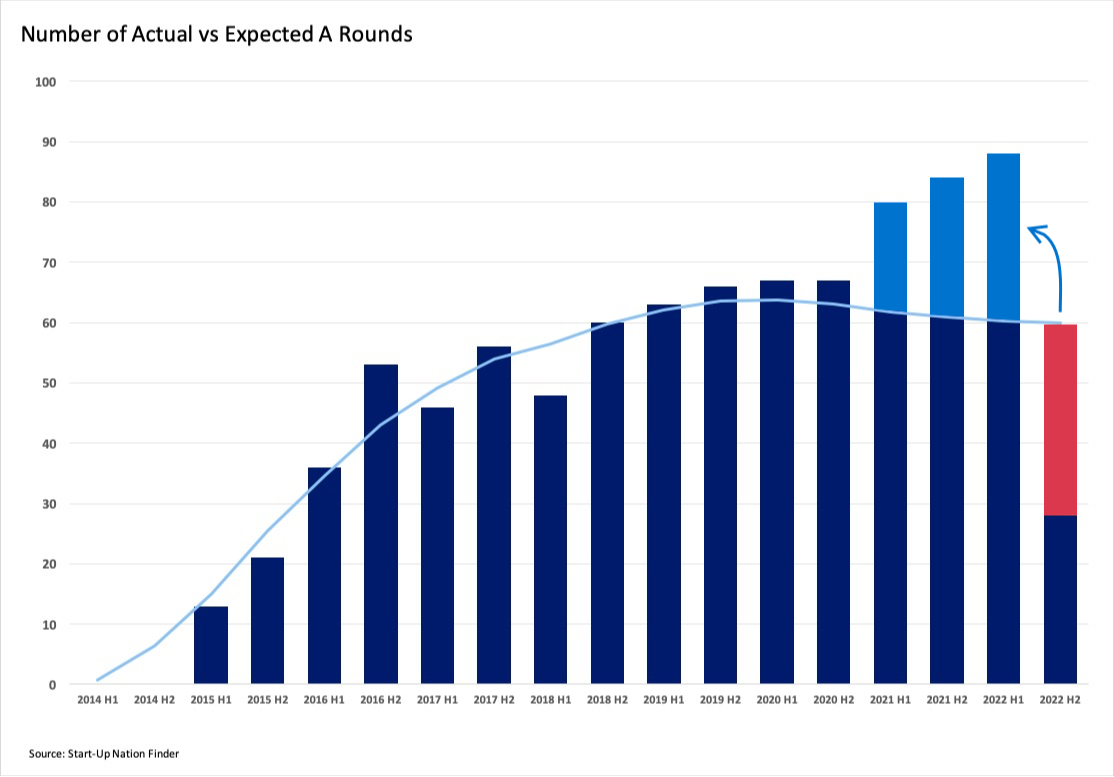

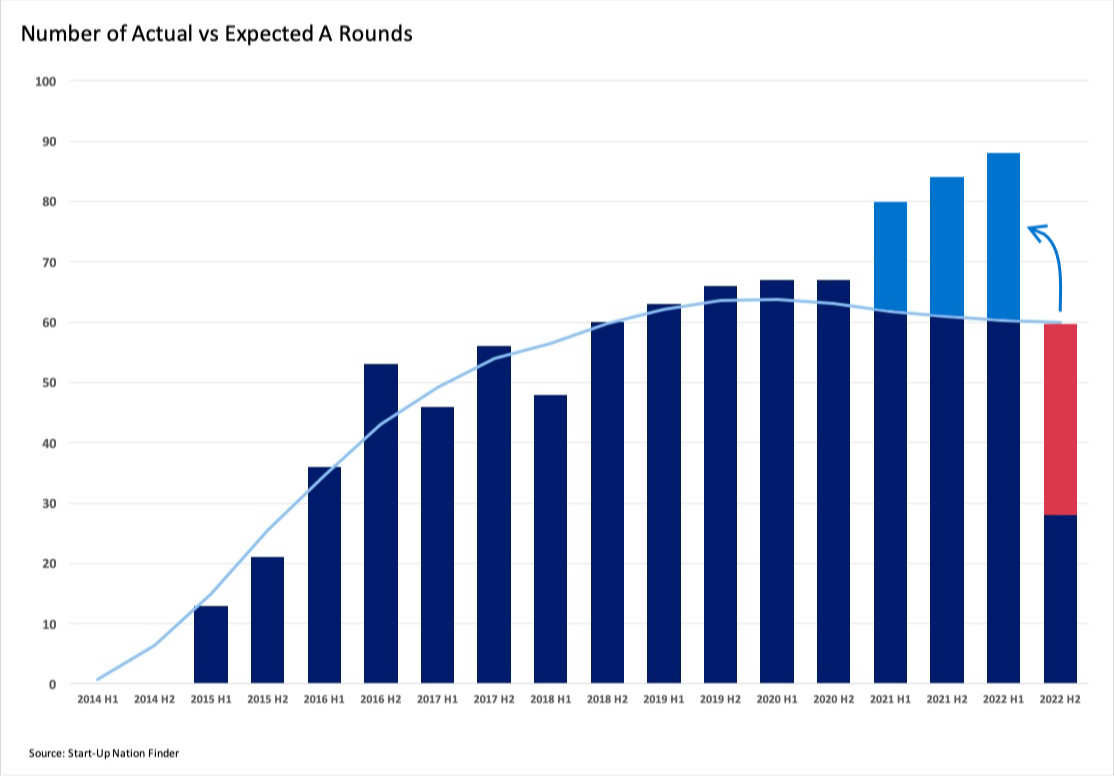

Based on historical data, we have built a statistical model of the duration of time between seed rounds and A rounds, while considering two important facts:

Only 40% of start-ups that raised seed funding succeed in raising A-round funding (this figure hardly varies among the different start-up cohorts).

Those start-ups that do succeed in raising A round funding take about three years to reach this milestone, but there is a considerable degree of variance (a standard deviation of 32 months).

Thus, the model must address the fact that for start-ups that have not yet raised A round funding, there is a decent probability that they will never do so, and this probability depends on the amount of time that has elapsed since the seed round.

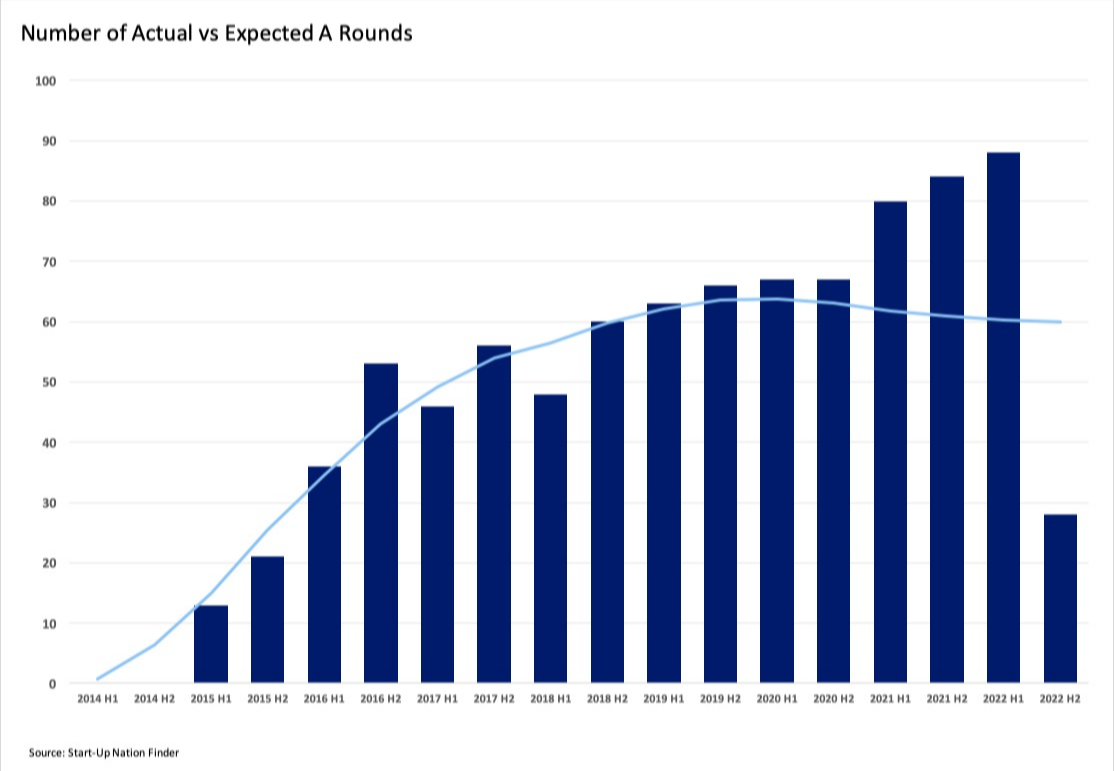

We estimated the model on all the companies raising seed funding between 2014 and 2017. We then compared the actual funding rounds to the model’s forecast for all companies that raised seed funding from 2014 to 2022.

Up until 2021, the model’s forecast matches the actual number of A rounds. Then in the three half-years starting in 2021, the number of A rounds was much higher than anticipated.

This is particularly true of those companies raising seed funding in 2020 and 2021; these companies, on average, raised A round funding earlier than the model expected.

Accordingly, these companies did not raise A rounds during the second half of 2022 simply because they had raised this funding round earlier – in 2021 and the first half of 2022.

Furthermore, it is clear that the surplus in funding created in the three half-years beginning in 2021 exceeds the “deficit” during the second half of 2022.

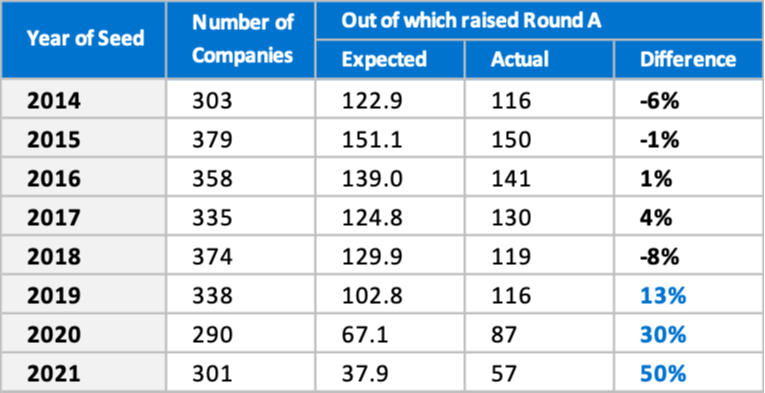

The bottom line is that the number of start-ups raising A rounds among all the cohorts is still similar to or higher than expected based on historical data, as shown in the table.

An alternative explanation for the reduced amount of time between the seed rounds and the A rounds is that there was an increase in the number of “successful” companies (in terms of their ability to raise A-rounds). An increase in the number of companies raising funds might be attributed to the a higher quality of companies in the last few years compared to their predecessors. Alternatively, it could be that investors lowered their quality threshold.

It will take a few years before we will be able to determine which of these explanations is more accurate. At this stage, however, there is no reason to assume that two consecutive start-up cohorts would suddenly be significantly more successful than those they preceded, especially considering that success rates have historically been stable. Moreover, if there has been a reduction in the quality threshold required for investment, we would expect to see a greater number of start-ups from the 2018 and 2019 cohorts succeed in raising funds (there are still some 200 companies in each cohort that have not yet raised A rounds).

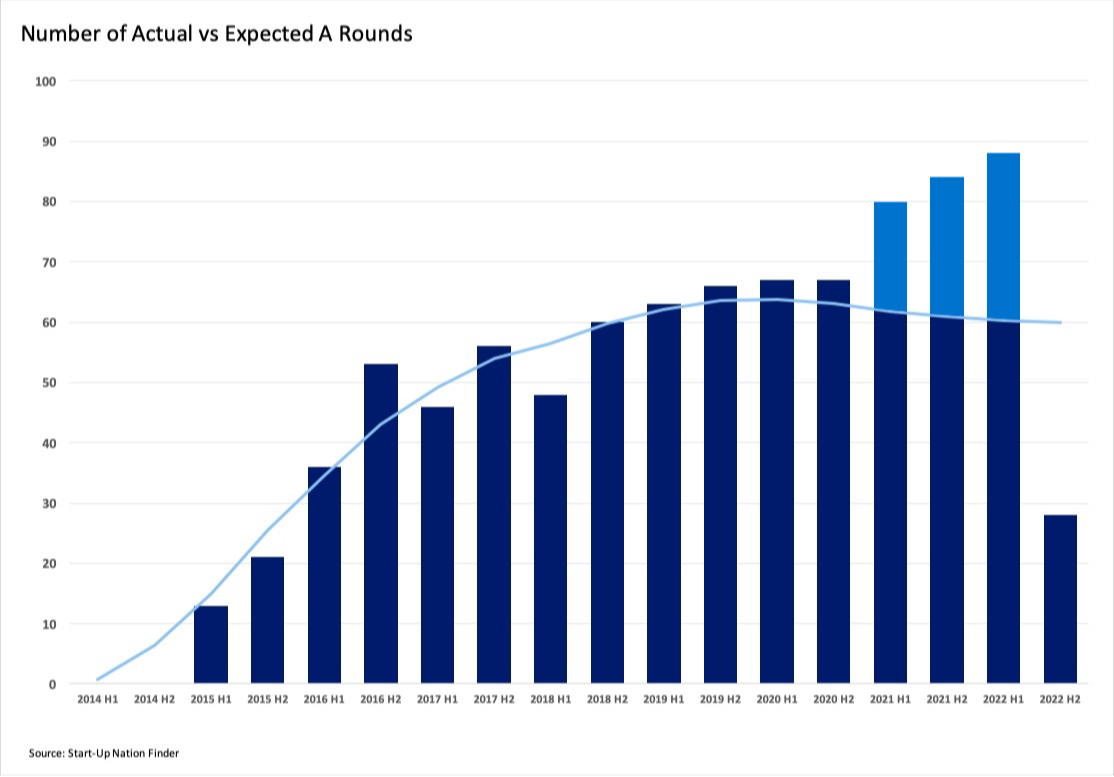

This analysis has also confirmed that the number of start-ups established in Israel in recent years is declining (this is reflected in the above figure by the downward trend of the red line since 2020, indicating that the model forecasts fewer A-rounds in recent years due to a decrease in the number of start-ups reaching seed stage). We warned about this trend in our previous reports (one of which was co-authored with the Israel Innovation Authority).

Up until 2021, the model’s forecast matches the actual number of A rounds. Then in the three half-years starting in 2021, the number of A rounds was much higher than anticipated.

This is particularly true of those companies raising seed funding in 2020 and 2021; these companies, on average, raised A round funding earlier than the model expected.

Accordingly, these companies did not raise A rounds during the second half of 2022 simply because they had raised this funding round earlier – in 2021 and the first half of 2022.

Furthermore, it is clear that the surplus in funding created in the three half-years beginning in 2021 exceeds the “deficit” during the second half of 2022.

The bottom line is that the number of start-ups raising A rounds among all the cohorts is still similar to or higher than expected based on historical data, as shown in the table.

An alternative explanation for the reduced amount of time between the seed rounds and the A rounds is that there was an increase in the number of “successful” companies (in terms of their ability to raise A-rounds). An increase in the number of companies raising funds might be attributed to the a higher quality of companies in the last few years compared to their predecessors. Alternatively, it could be that investors lowered their quality threshold.

It will take a few years before we will be able to determine which of these explanations is more accurate. At this stage, however, there is no reason to assume that two consecutive start-up cohorts would suddenly be significantly more successful than those they preceded, especially considering that success rates have historically been stable. Moreover, if there has been a reduction in the quality threshold required for investment, we would expect to see a greater number of start-ups from the 2018 and 2019 cohorts succeed in raising funds (there are still some 200 companies in each cohort that have not yet raised A rounds).

This analysis has also confirmed that the number of start-ups established in Israel in recent years is declining (this is reflected in the above figure by the downward trend of the red line since 2020, indicating that the model forecasts fewer A-rounds in recent years due to a decrease in the number of start-ups reaching seed stage). We warned about this trend in our previous reports (one of which was co-authored with the Israel Innovation Authority).

OurCrowd and Viola (all funds) were the most active Israeli investors in 2022. OurCrowd invested in 84 different start-ups, while Viola was involved in 47. They are followed by Pitango, which invested in 21 different start-ups.

Out of the foreign VCs operating in the Israeli ecosystem, Insight Partners was the most active in 2022 funding 40 different start-ups. Tiger Global was the second most active and invested in 26 start-ups.

When Tiger first started investing in Israel, they concentrated only on late-stage rounds, but they recently announced that they are turning some of their attention to seed stage funding as well. As mentioned earlier, in 2022, they invested in only three seed rounds.

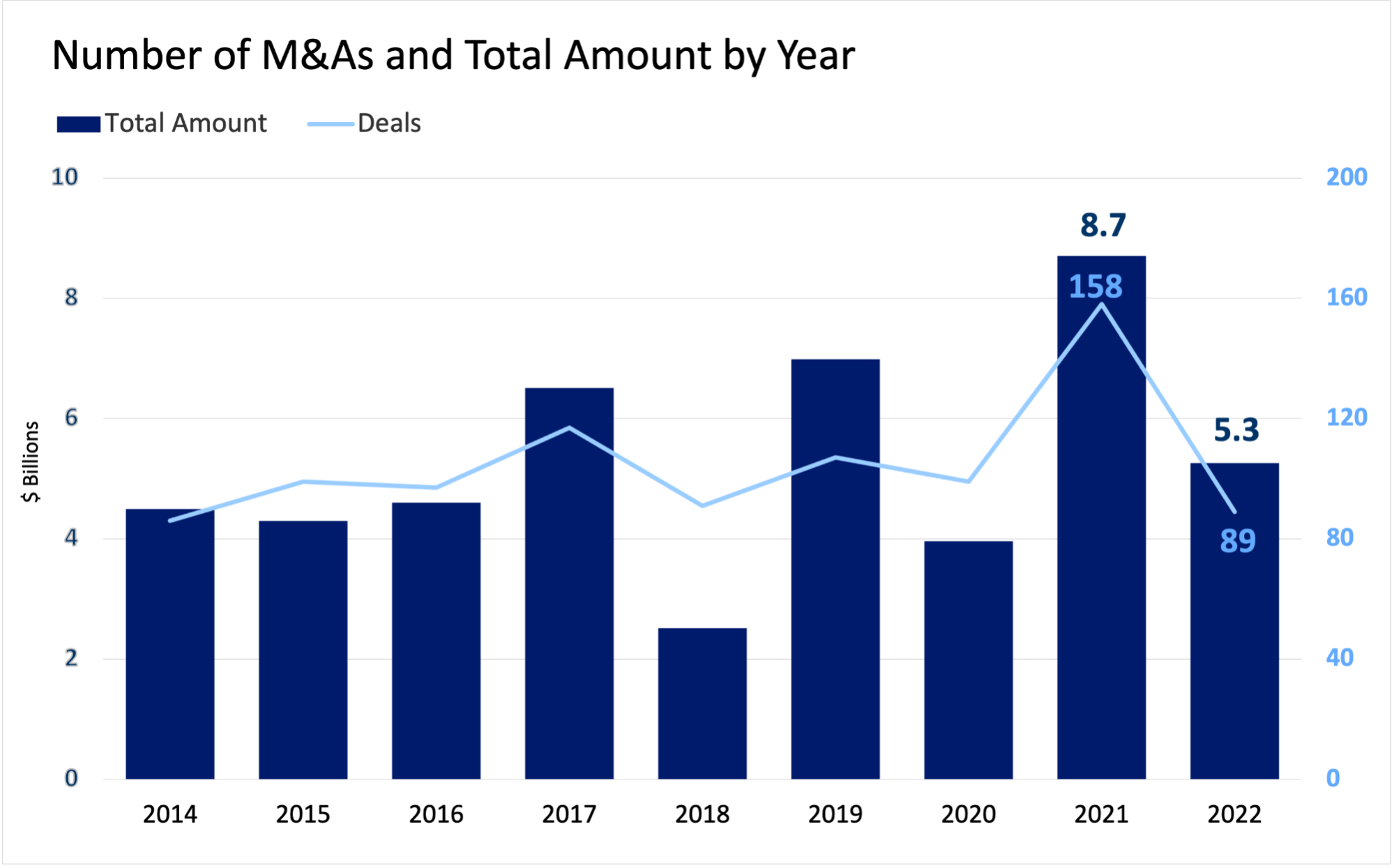

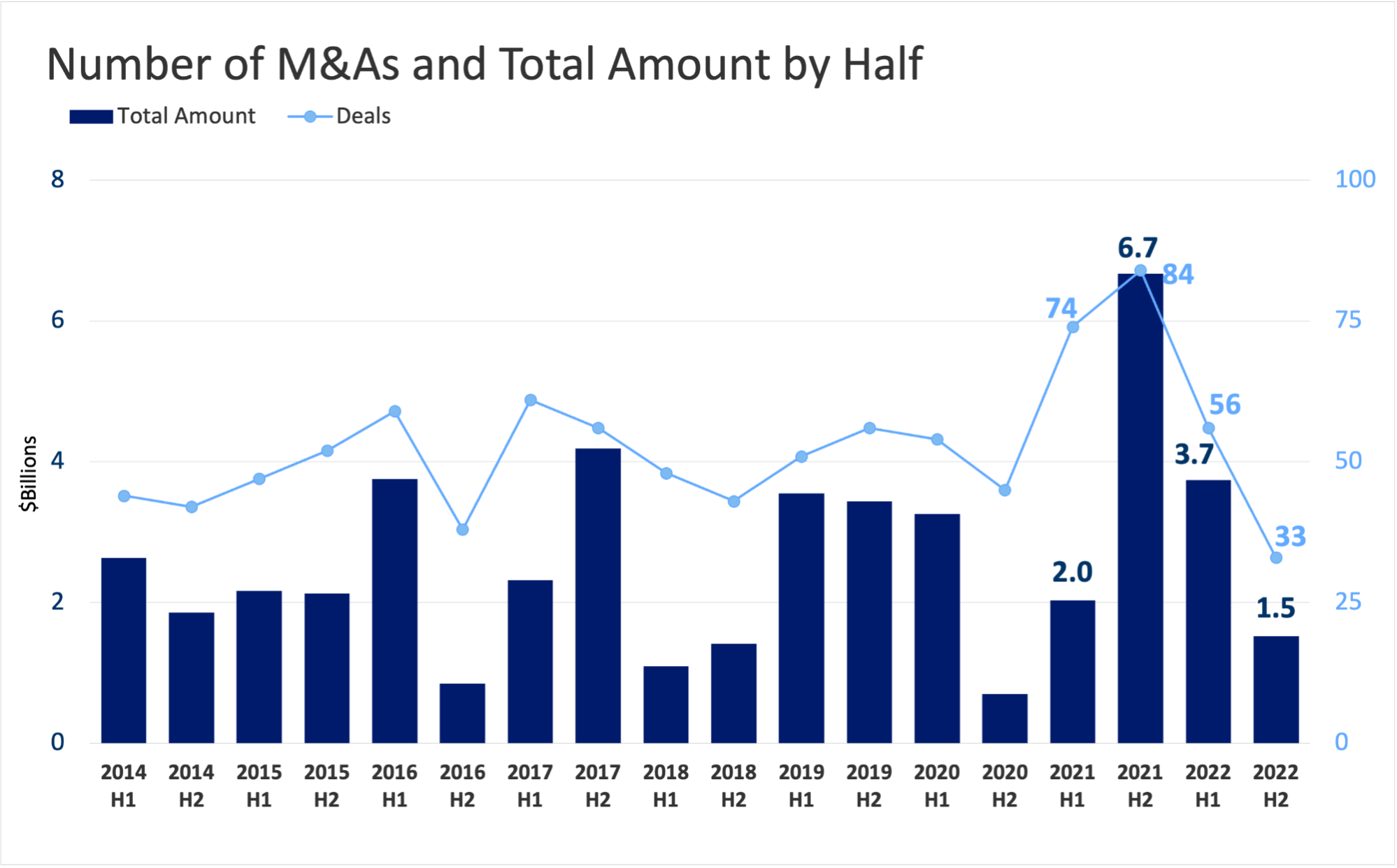

In comparison to the previous year,2022 saw 45% decrease in the number of first time M&As and of 40% in their overall sum, as shown in Graph 9. Eighty-nine companies were sold for a total sum of USD 5.3 billion. Below are some of the most notable acquisitions: (all of which occurred between March and May) being:

Granulate, acquired by Intel for USD 650 million

Finaro, sold to Shift4 for USD 575 million

Zimperium, sold to Liberty Strategic Capital for USD 525 million

Looking at the number of first time M&As per half year, the slowdown during the second half of 2022 is particularly notable. The number of M&As during the last half year was the lowest in recent years, and their overall amount was the fourth lowest recorded in the Finder database.

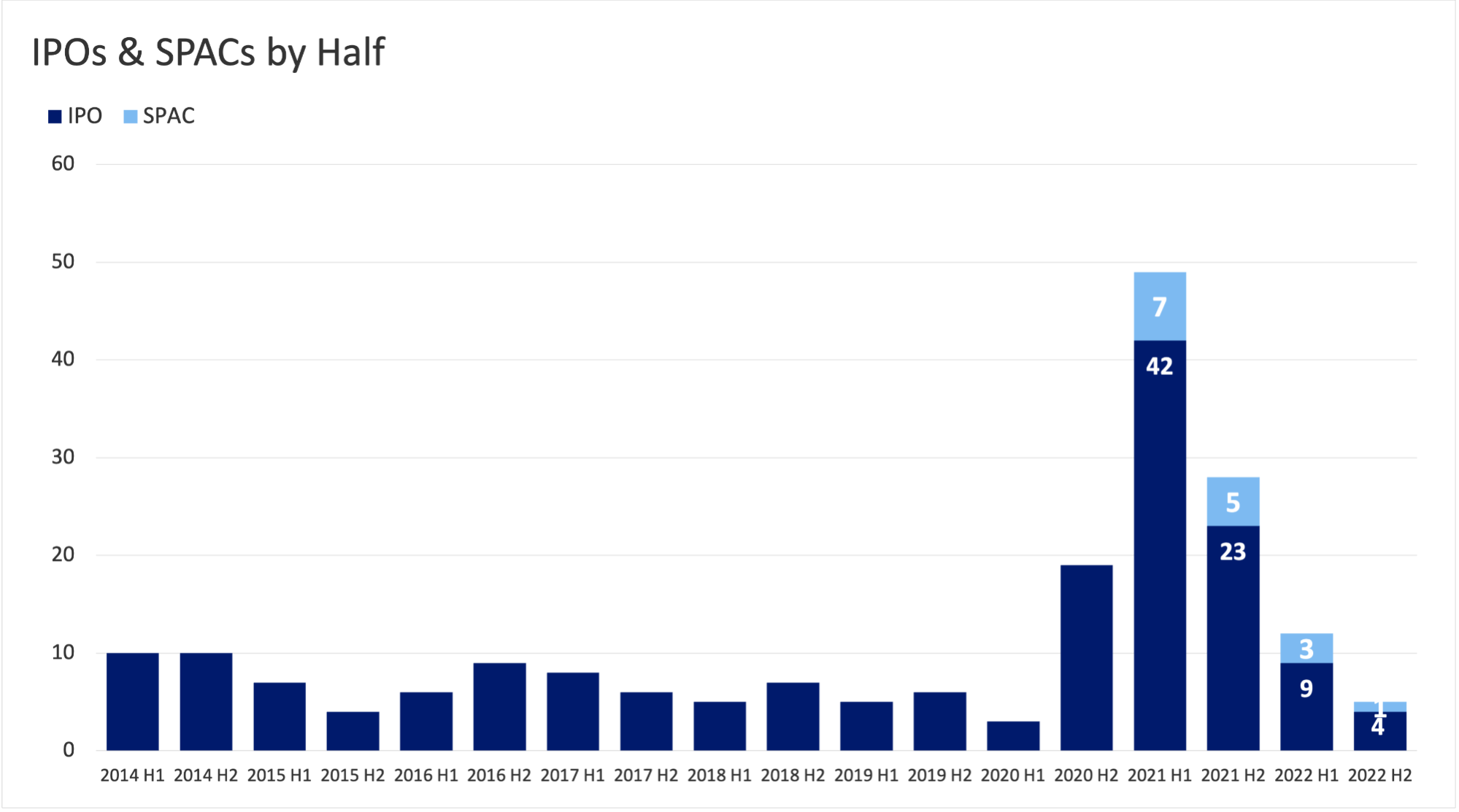

In 2022, 13 companies went public, with an additional four companies doing so via SPACs. On the one hand, this represents a drastic reduction compared to the record number of 77 IPOs (including SPACs) that took place in 2021; on the other hand, it represents a return to the “normal” numbers (between 10 and 20 new IPOs annually) to which the Israeli high-tech industry is accustomed.

As in previous sections, there is a significant difference between the two halves of 2022: there were only five IPOs in the second half of the year, one of which was a SPAC. This figure is hardly surprising given the weakness of the financial markets.

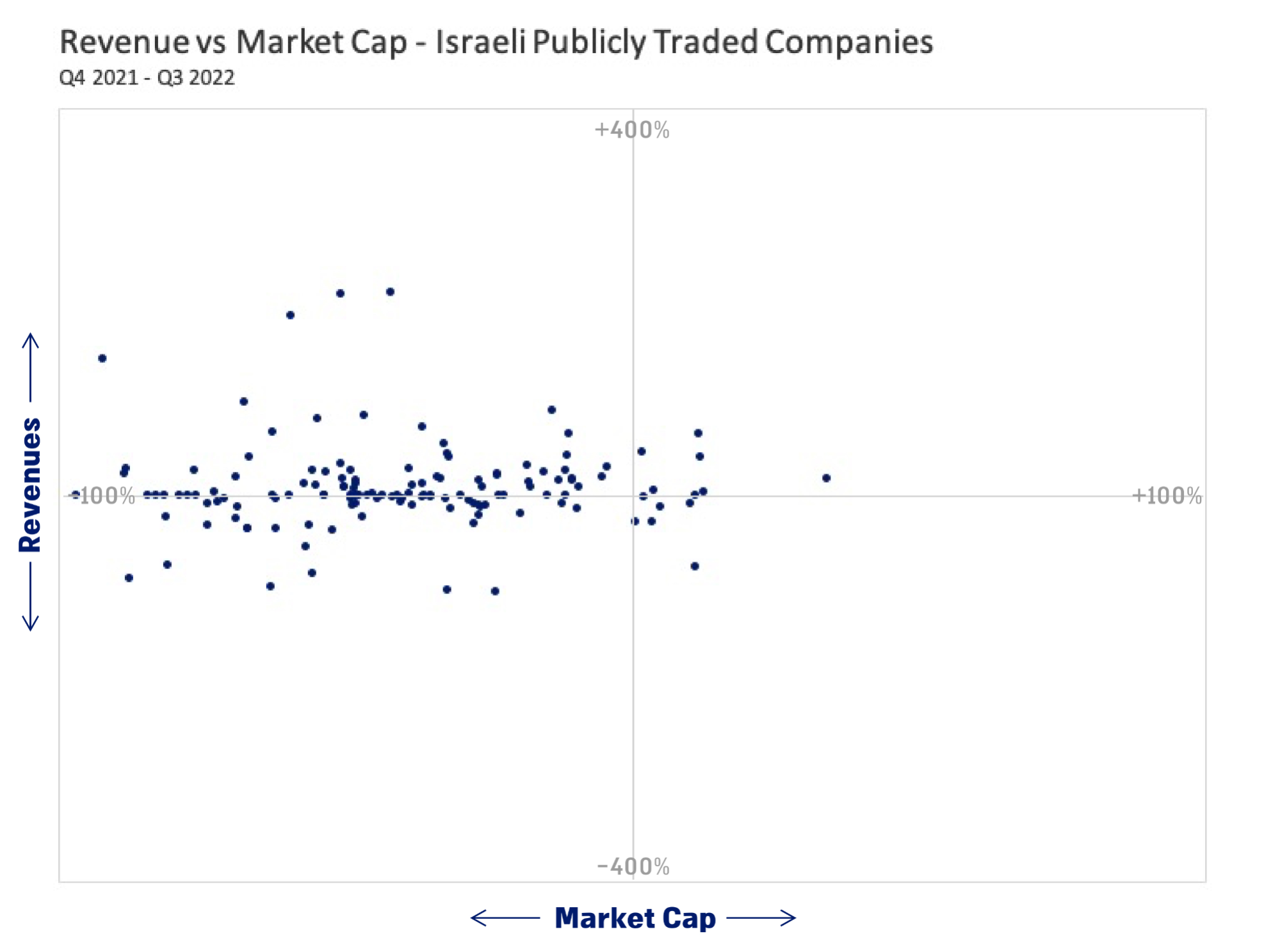

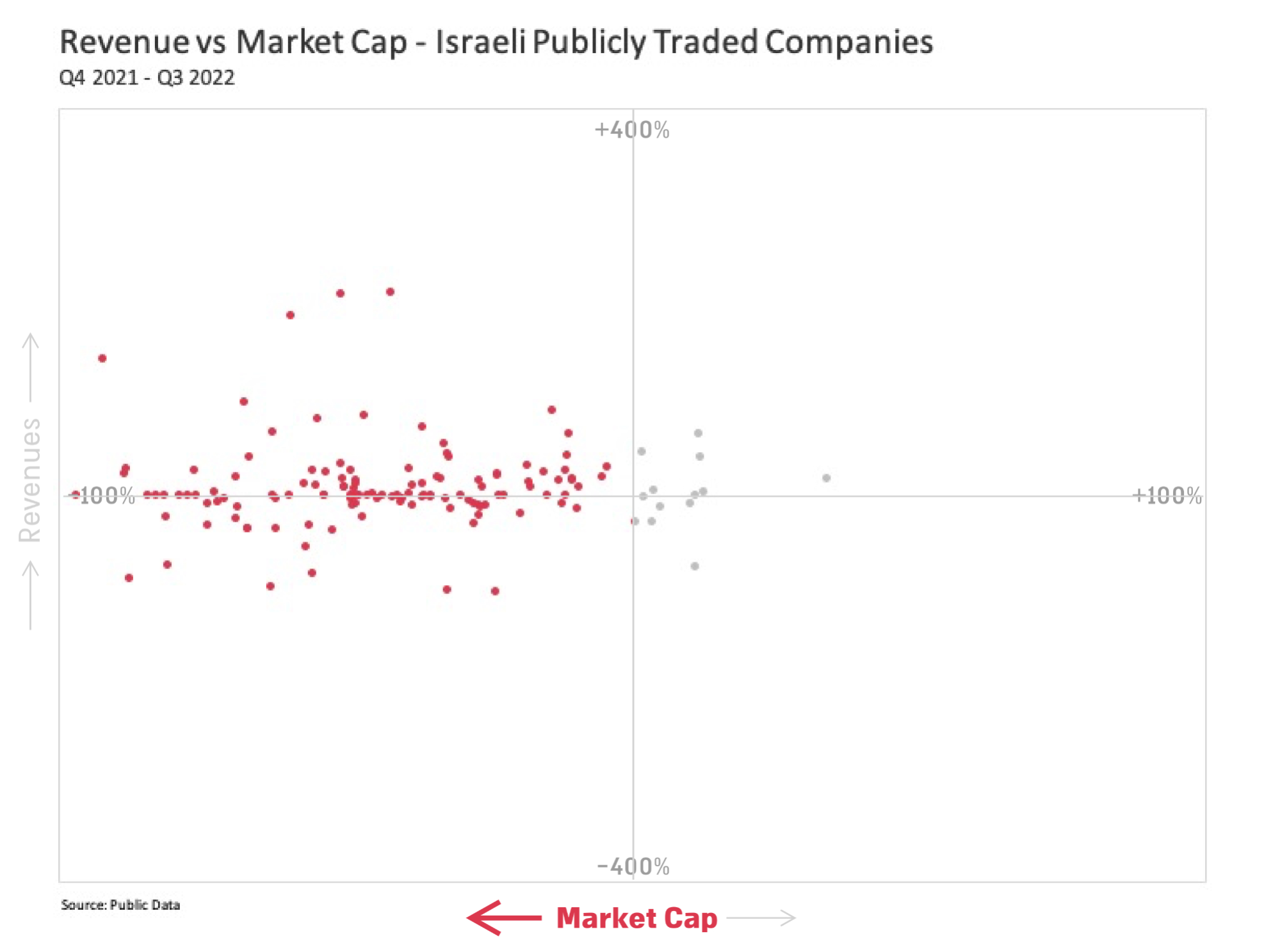

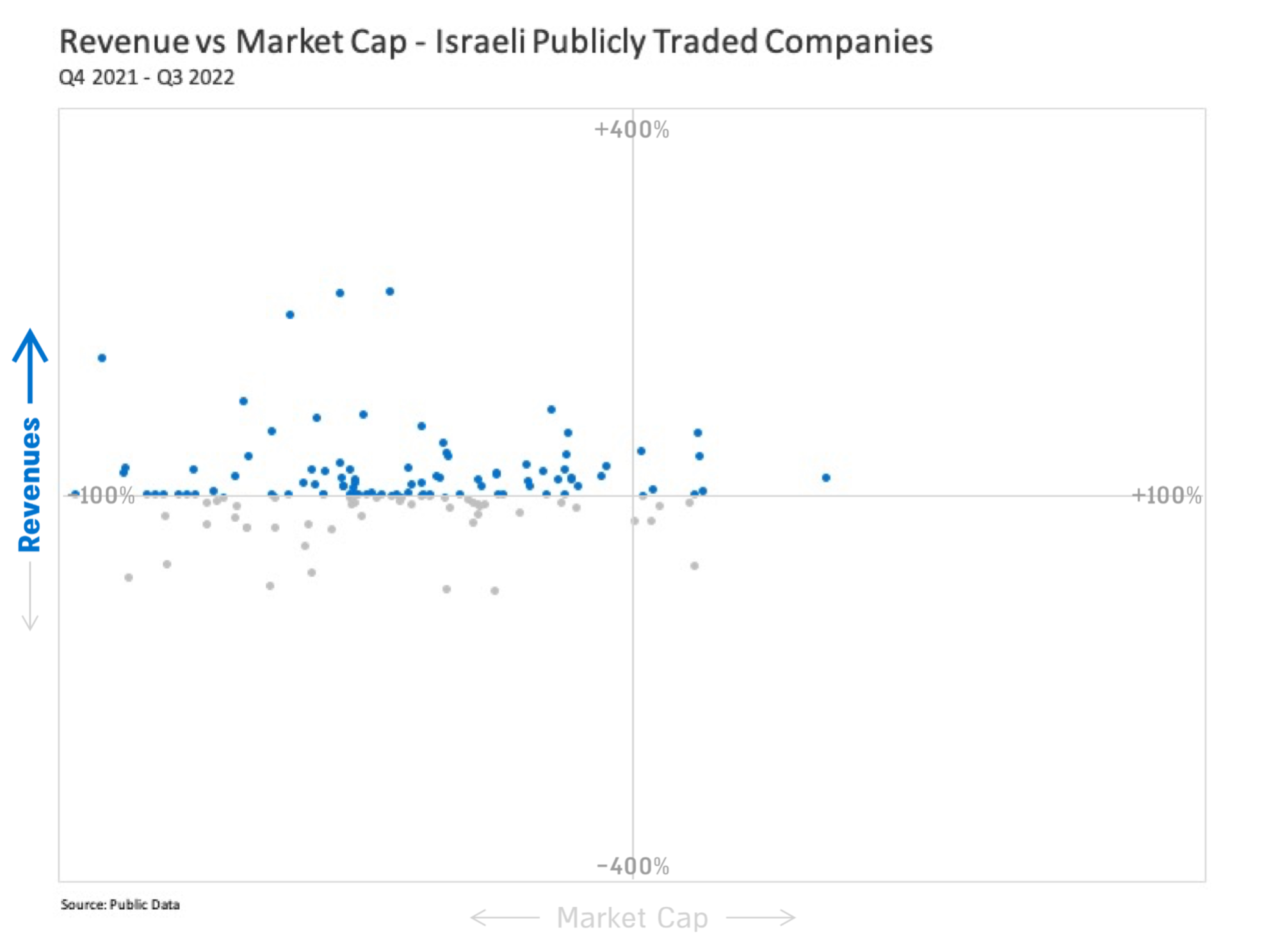

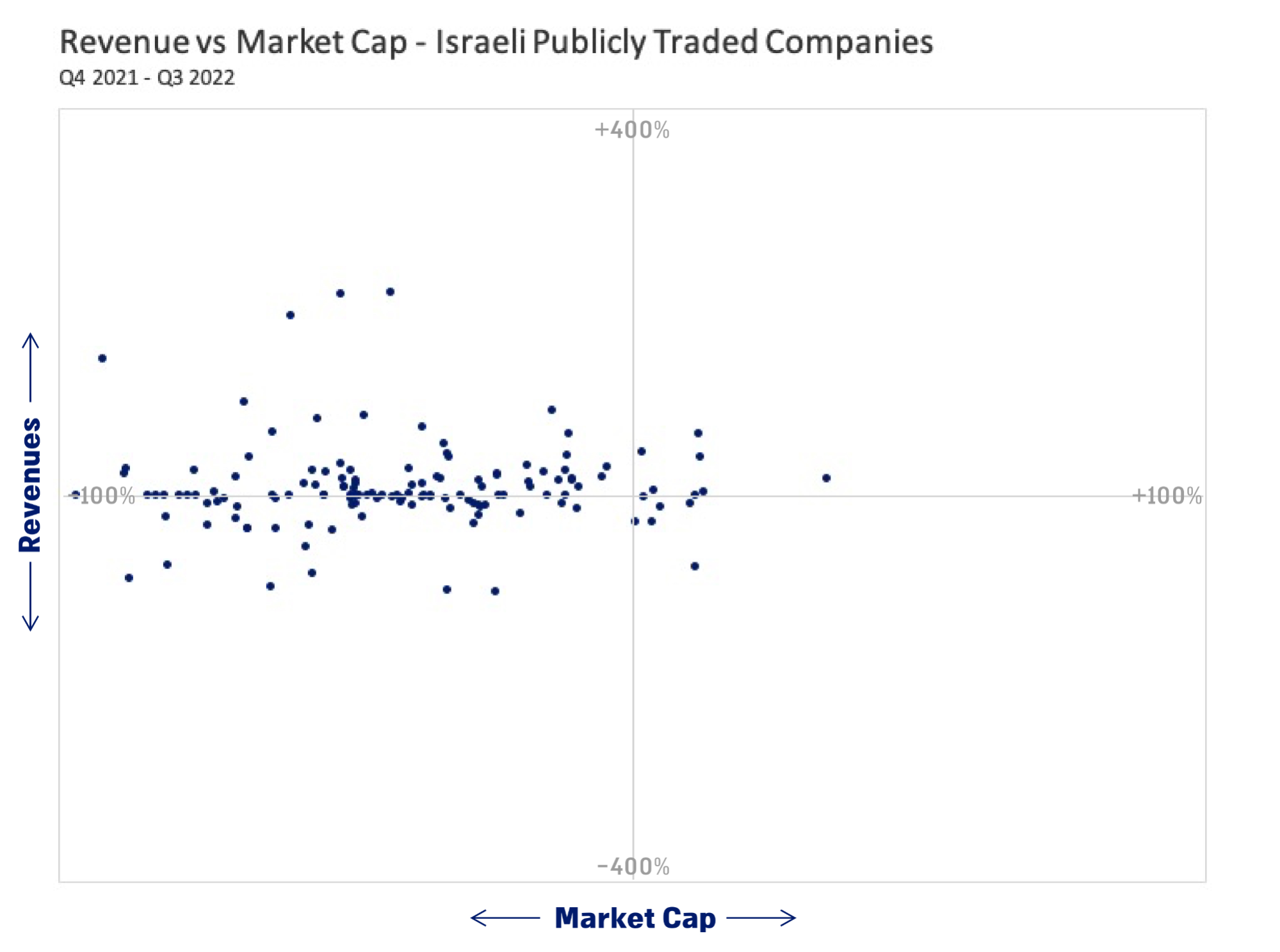

Given the decline in companies’ share prices in all major stock exchanges, a phenomenon which was more pronounced for technology companies, we examined whether the decline also linked also to company performance.

Using the companies’ financial statements, we examined the change in their revenues between Q4 2021 and Q3 2022 (the most up-to-date statistic available to us at the time of writing the report). The horizontal axis depicting the percentage change in market capitalization (market cap) and the vertical axis showing the percentage change in revenue between the quarters in question.

an overwhelming majority, 107 compared to 12 of the Israeli publicly traded companies recorded a decline in their market cap

Among the companies examined, the majority of companies, 69 compared to 0, actually experienced an increase in revenues between the relevant quarters.

We found no correlation between these variables, which indicates that the decline in market cap was the result of macroeconomic factors rather than the companies’ performance.

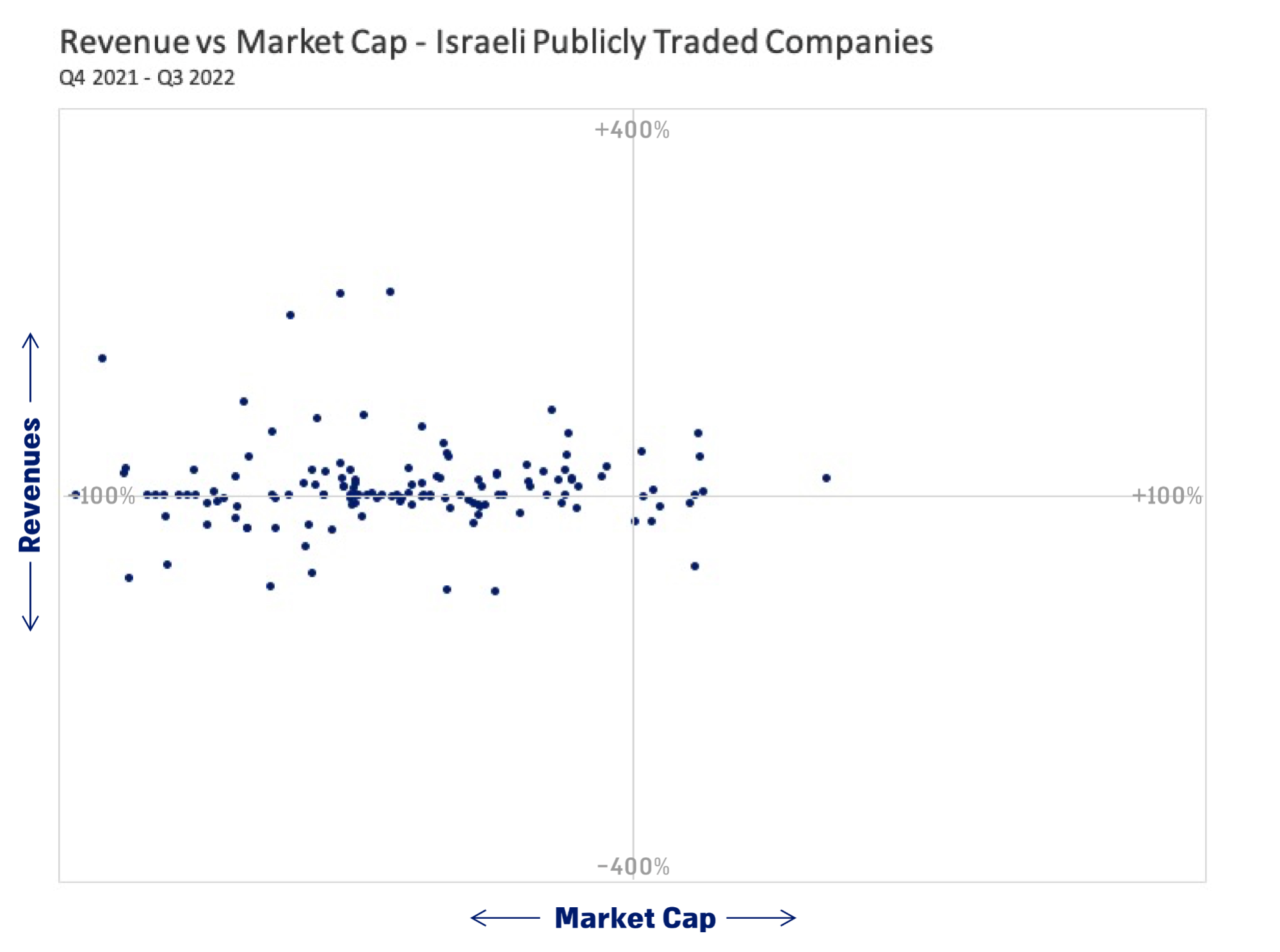

Given the decline in companies’ share prices in all major stock exchanges, a phenomenon which was more pronounced for technology companies, we examined whether the decline also linked also to company performance.

Using the companies’ financial statements, we examined the change in their revenues between Q4 2021 and Q3 2022 (the most up-to-date statistic available to us at the time of writing the report). The horizontal axis depicting the percentage change in market capitalization (market cap) and the vertical axis showing the percentage change in revenue between the quarters in question.

an overwhelming majority, 107 compared to 12 of the Israeli publicly traded companies recorded a decline in their market cap

Among the companies examined, the majority of companies, 69 compared to 0, actually experienced an increase in revenues between the relevant quarters.

We found no correlation between these variables, which indicates that the decline in market cap was the result of macroeconomic factors rather than the companies’ performance.

The startups in the Finder database are divided into 11 sectors.

As in previous years, the leading sectors in terms of investment were software based, primarily Enterprise Software, Security Tech (which includes Cyber) and FinTech.

In most sectors, there is a clear correlation between their share of the overall amount of funds raised and their share of the total number of deals. On the other hand, while FinTech accounts for nearly 10% of all the transactions, it attracted more than 15% of VC investments.

In the Agri & Food-Tech sector, the opposite is true, with the sector accounting for 10% of the transactions but attracting only 5% of the VC investments.

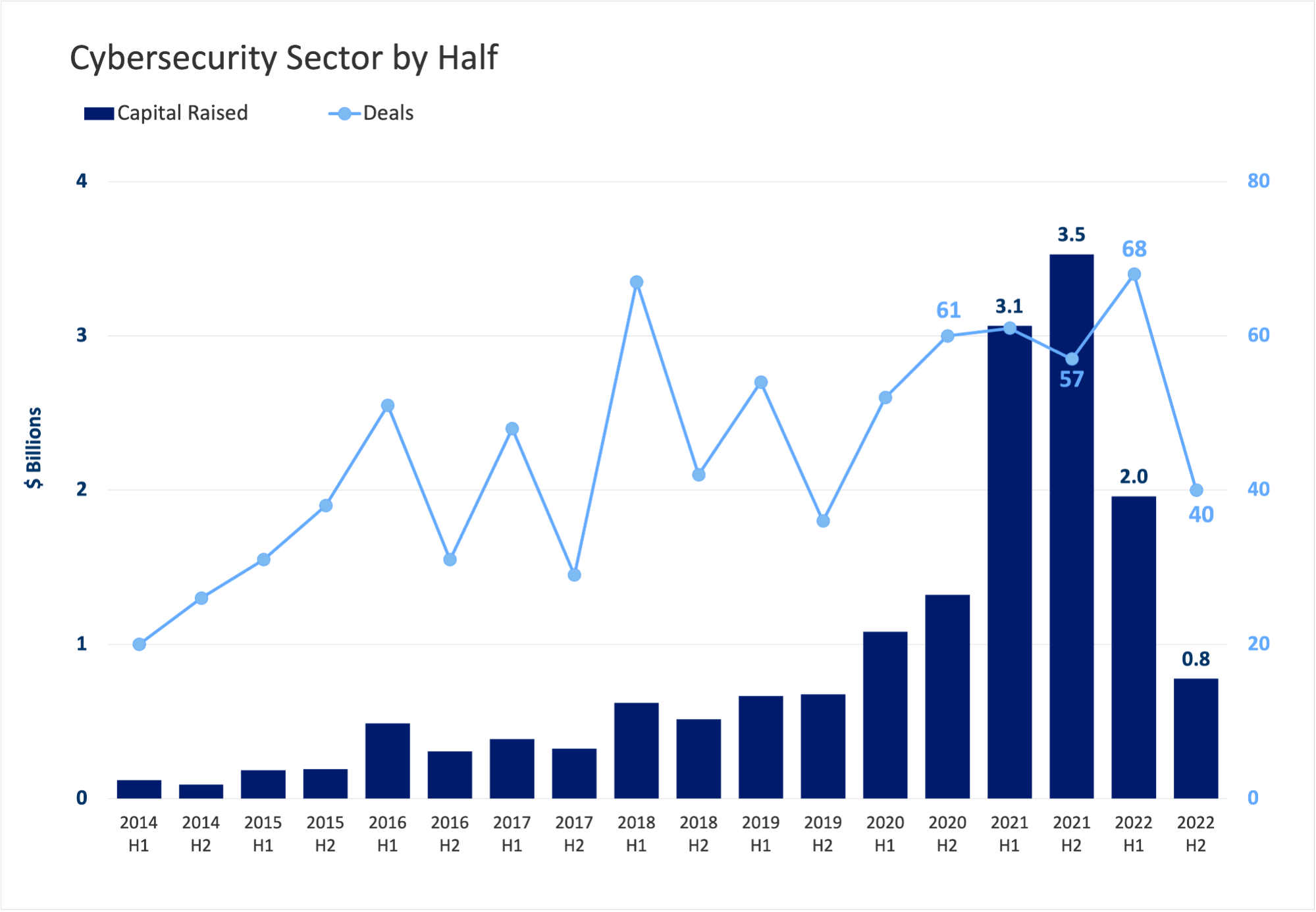

As of late 2022, there are 676 active cyber companies in Israel, which are divided into the following main sub-sectors (some of the companies belong to more than one sub-sector): data protection, network security, cloud security, app security, endpoint security, and risk & GRC management.

There was a 60% decrease in the total amount in this sector between 2021 and 2022, compared to an industry-wide decline of 42%. That said, the number of funding rounds was stable compared to 2021.

The distribution into half-years helps to understand this trend, as in both halves of 2022 there was a significant decline in the overall amount of capital raised. The number of funding rounds during the first half of 2022 was larger than in 2021, but the second half of 2022 saw a significant decrease.

Read more +

The key investors in this sector in 2022 include: Insight Partners, which was involved in nine different startups last year and Tiger Global and Glilot Capital Partners, with eight investments each.

During 2022, there were 20 exits of Israeli cyber companies. The largest acquisition was that of Zimperium, which was acquired by the British investment fund, Liberty Strategic Capital, for USD 525 million. The second largest acquisition was that of the Israeli cyber company Medigate by Claroty for USD 400 million. The third largest was Palo Alto’s acquisition of Cider Security for USD 300 million.

To date, there are 441 companies in this sector, divided into the following spheres (some startups may belong to more than one field):

139 startups engaged in commerce and investment

126 dealing with money transfers

82 startups engaged in optimization and loans

79 dealing with independent financial management

62 Insurtech companies

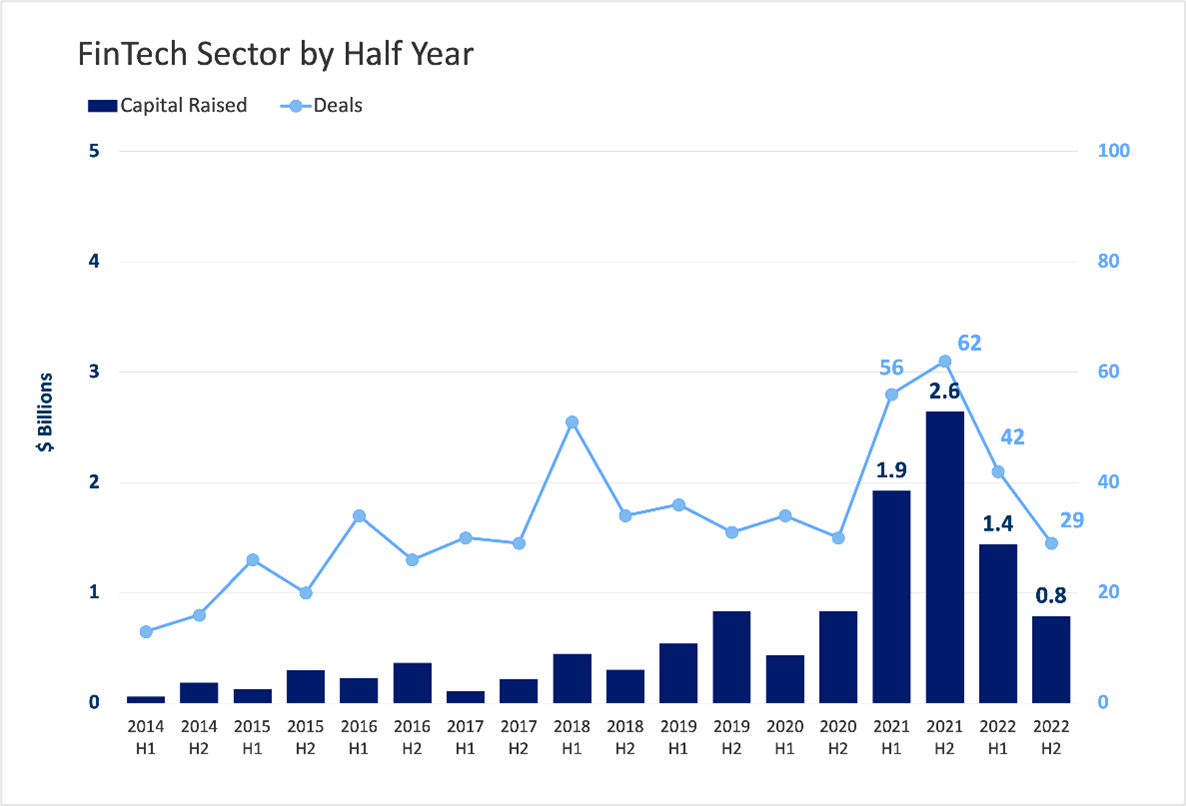

The 51% decline in the amount invested in this sector is similar to that of the entire industry, and despite a similar decline in the funding rounds compared to 2021, the number of rounds remains more or less identical to 2019–2020.

When looking at both halves of 2022, it appears that the decline in the deal count amounts to 31%, and the total amount of funding has been decreased by 45%.

Read more +

The most noteworthy investors in 2022 include Viola (all funds), which invested in investing in 13 startups throughout the year. The American venture partner Lightspeed, and the Israeli VC OurCrowd, each invested in four different startups.

This year there were a total of four exits. The most notable of these was the SPAC merger of Pagaya in June and the sale of Finaro to the publicly traded company Shift4 for USD 575 million.

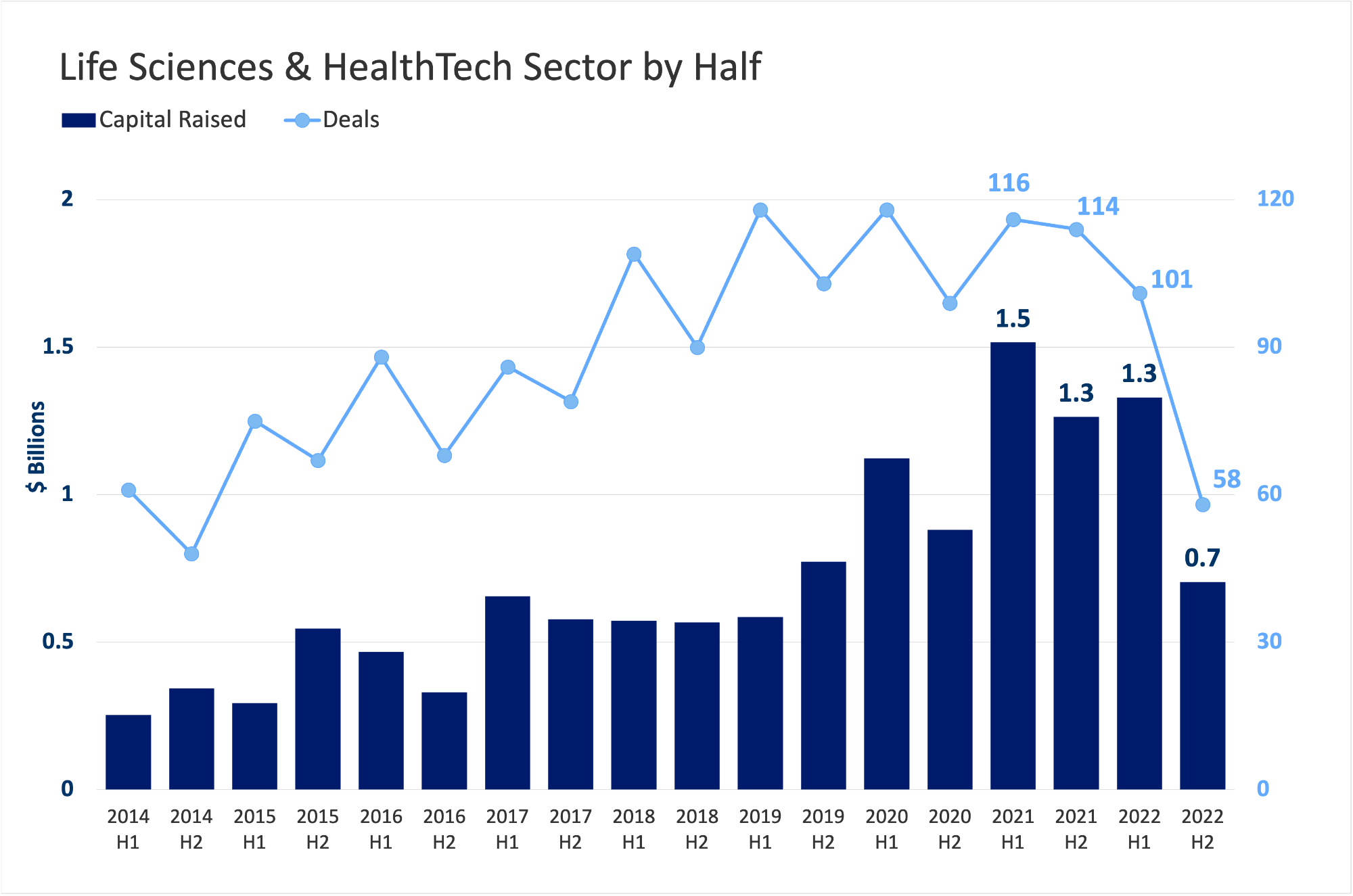

There are 1,578 active companies in the Life Sciences and HealthTech sector as of 2022. These companies are divided into three main sub-sectors (some of the companies belong to more than one sub-sector):

Digital health (mainly software-based services and health service platforms) – 700 companies

Development and manufacture of medical devices – 606 companies

Pharma and biomedicine – 451 companies

In 2022, startups in these sectors raised USD 2.0 billion, representing a relatively modest decline of 27% compared to 2021. At the same time, the number of funding rounds was the lowest since 2016, mainly to the second half of the year, which saw the lowest number of funding rounds since 2014.

Read more +

The largest investors in this sector in 2022 are OurCrowd, which been invested in 20 different startups and eHealth Ventures, which was active in seven startups. They are followed by the Israeli fund aMoon and the American VC Insight Partners, which each invested in six different startups. Five exits were recorded in this sector in 2022, the most prominent being Shamir Optical Industry, Perflow Medical, and the IPO of Stickit Labs.

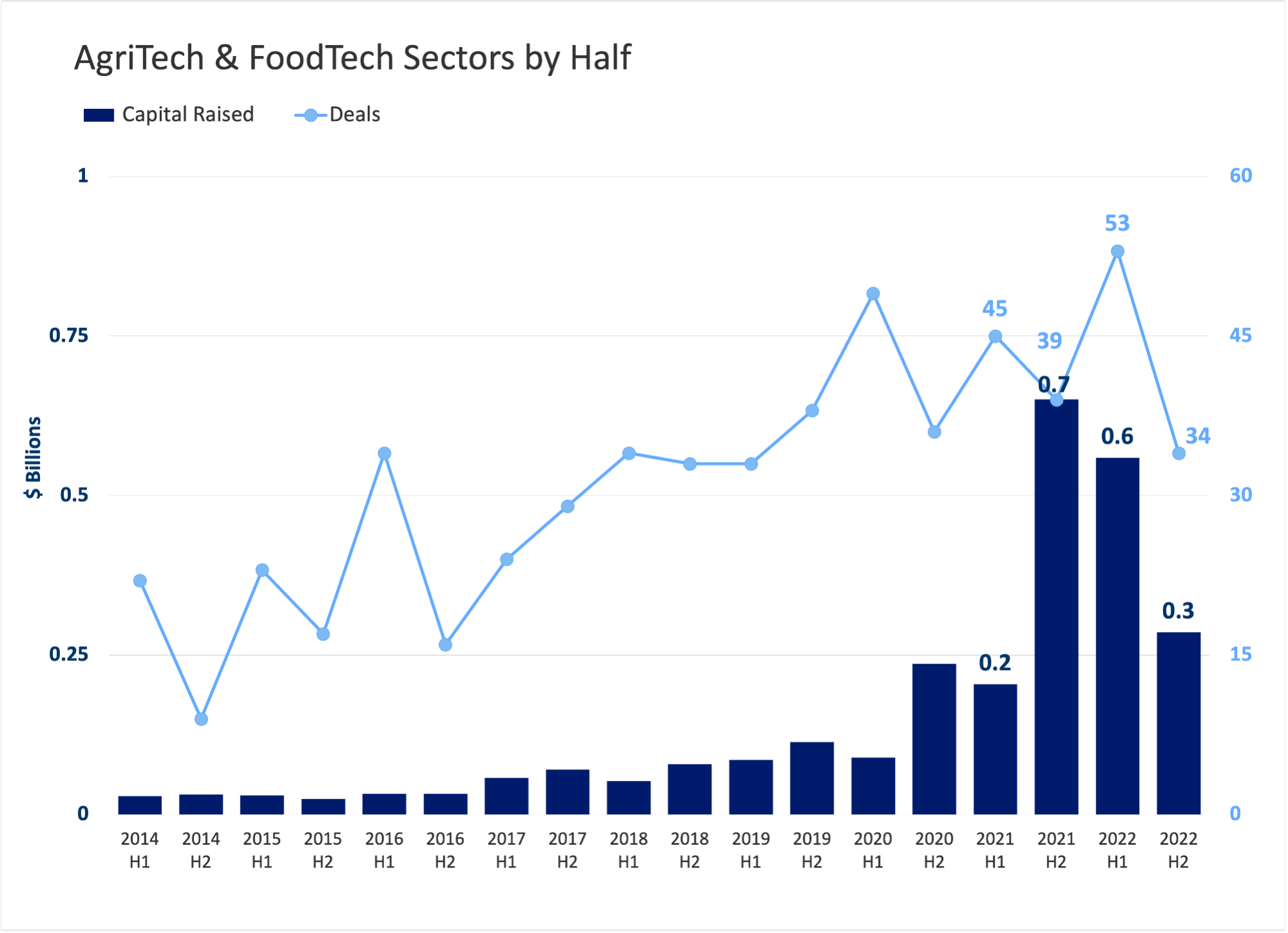

This sector is relatively small but has been experiencing rapid growth in recent years. As of late 2022, there were 624 active startups in this sector, divided into the following sub-sectors (some startups may belong to more than one field):

167 startups dealing with irrigation-related innovation

160 startups in the field of yield optimization harvest

104 alternative food startups

72 startups involved in the food production chain

64 pest pathogens startups

63 in agricultural inputs

45 in produce preservation and trade

This is the only sector that shows an increase in the number of funding rounds between 2021 and 2022, and a firm stability in the total amount of funding. Given the possibility of additional funding rounds that have yet to be revealed, it is possible that the total volume of investments here will be even greater than that of the previous year.

Examining the investment figures in greater detail, one can see a slight rise in investment amounts beginning in the second half of 2020. Despite the decline in the second half of 2022, the investment figures are still relatively high vis-à-vis historic figures.

Read more +

Notable investors in this sector included OurCrowd, which participated in the largest number of funding rounds in 20 different startups. It came as no surprise that the two incubators, The Kitchen and Fresh Start, were also among the leading investors, with five investments each.

In 2022, no exits were recorded in this sector.

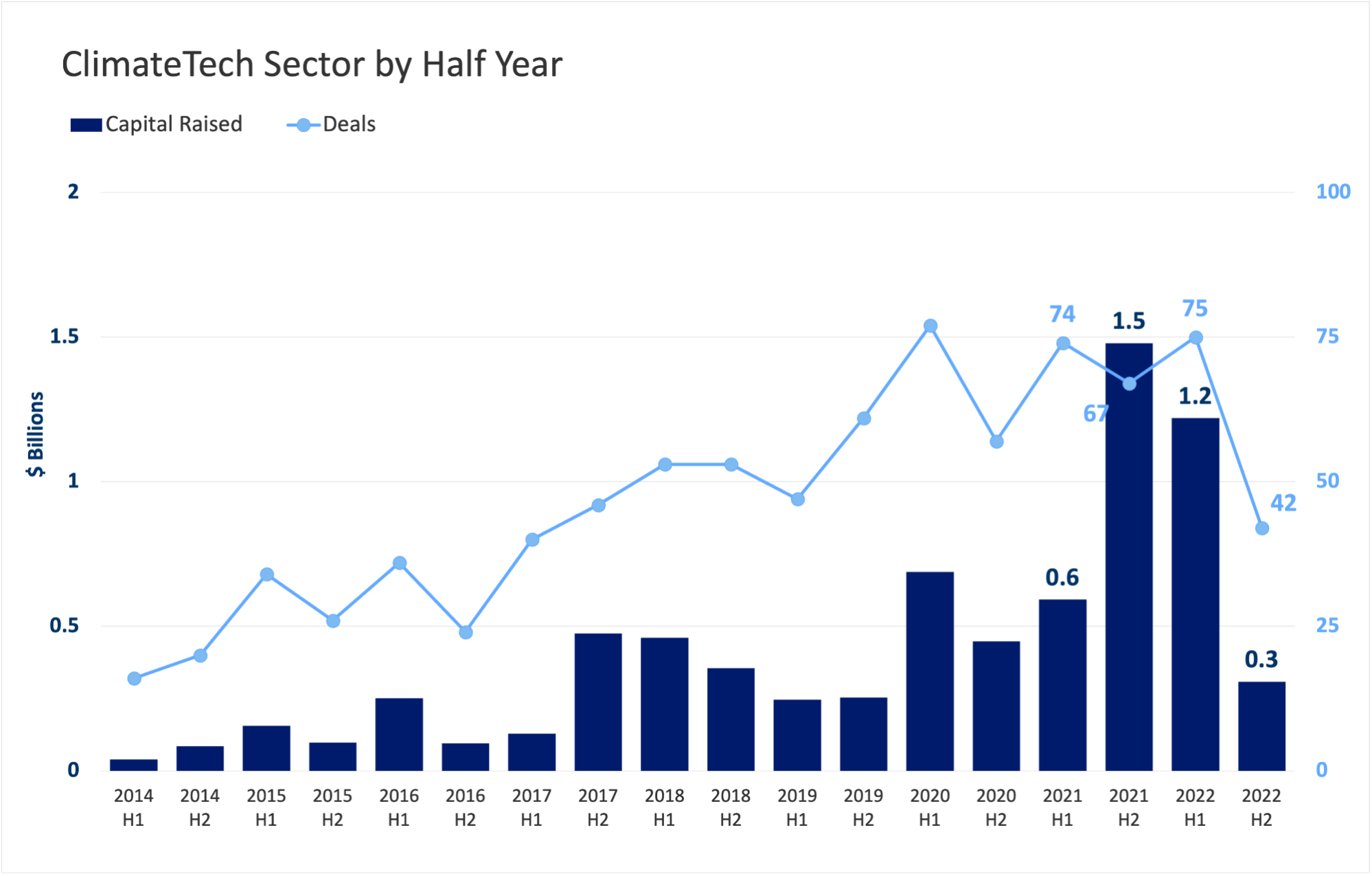

This sector is not part of the standard sectors division in the Finder database, mainly because engaged in this “sector” operate in diverse fields. As of late 2022, there are over 800 companies active in this sector. In 2022, there was a decrease in the overall amount of capital raised; USD 1.5 billion in 117 funding rounds. Although this represents a 26% decrease compared to the previous year, in which USD 2.1 billion was raised, this still constitutes an overall trend of growth since 2014 (apart from 2019), when Climate-Tech became prominent and began to attract global attention.

A Comparison of the two halves of 2022 shows that during the first half of the year, the amount of investment was higher than the average and was essentially a direct continuation of 2021, while during the second half of the year, the amount of investment plummeted by 75%.

Read more +

The most prominent investors in this field in 2022 are OurCrowd, with investments in 14 different startups, followed by Capital Nature with seven investments, and Insight Partners with six investments. Firstime VC in five startups and Doral Energy Tech Ventures invested in four startup.

This year, there were a total of five exits, the most notable being the sale of BreezoMeter to Google for USD 200 million.

Start-Up Nation Central is a non-profit organization that connects Israeli innovation to the world in order to help international entities solve global challenges. Immersed in the Israeli technology ecosystem, we provide a platform that nurtures business growth, recommends policies, and generates partnerships with corporations, governments, investors, and NGOs to strengthen Israel's economy and society.

Start-Up Nation Finder is the free digital platform to learn about and engage with the Israeli tech ecosystem. Finder provides data, insights, and access to key industry players, enabling users to create business value through collaborations.

Start-Up Nation Policy Institute is an independent think-tank that works to strengthen the Israeli innovation ecosystem through research and policy recommendations. The Institute works in partnership with the public sector and the high-tech industry to advance policies that maintain Israel’s technological edge and expand Israeli innovation to all areas of its economy & society. The Institute is part of the Start-Up Nation Central group and is fully funded by philanthropy.