The scale and scope of creators and the creator economy is large – and it’s growing. The influencer marketing industry is valued at $16.4 billion. Global creator marketing spend will exceed $24.1 billion by 2025.

The creator economy has expanded rapidly in recent years. There are now estimated to be 50 million content creators globally. 46.7 million consider themselves to be amateurs, and 30 million of them share their creativity on Instagram. More than 2 million consider themselves to be professional creators and more than 25% of them are mostly active on Instagram.

30% of 18 to 24-year-olds and 40% of 25 to 34-year-olds consider themselves content creators. 3.32% Instagrammers have more than 100,000 followers.

The average age of creators is 40, with Gen-Z (age 24 and younger) making up just 14% of all creators. More than half of creators are male (55%), though women outnumber men by nearly 2-to-1 when it comes to being full-time professional creators.

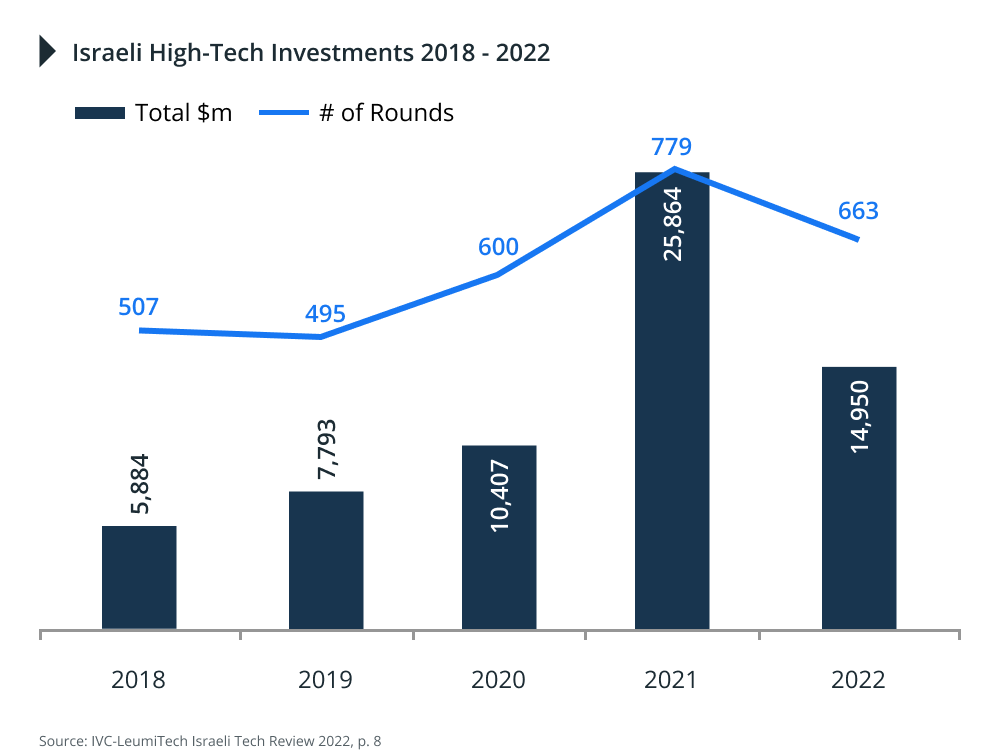

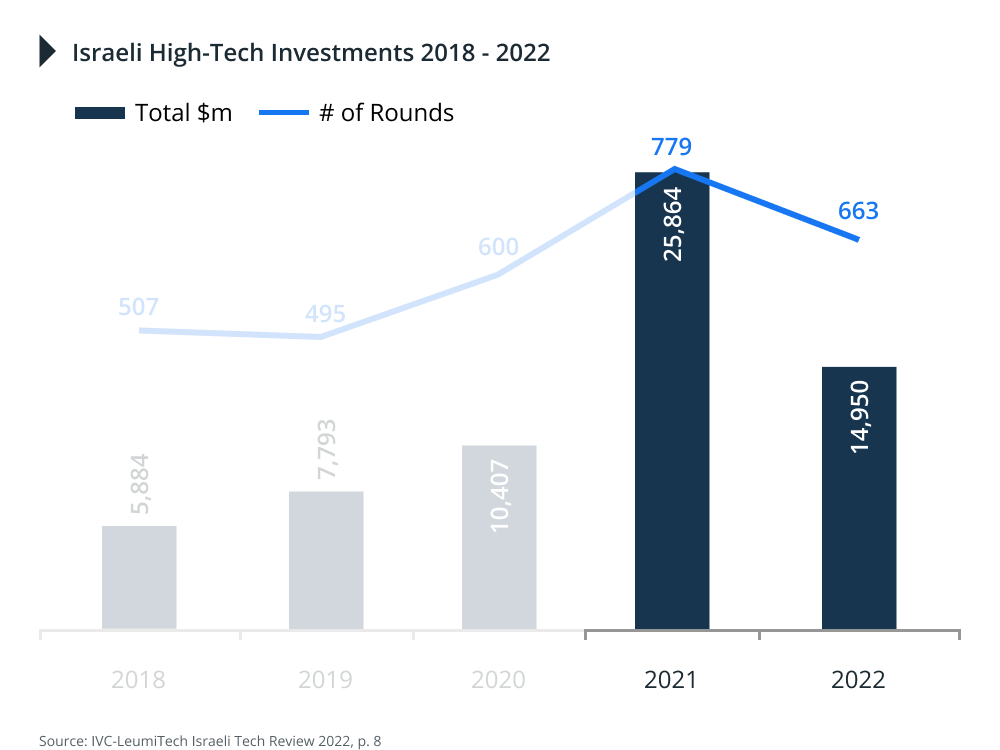

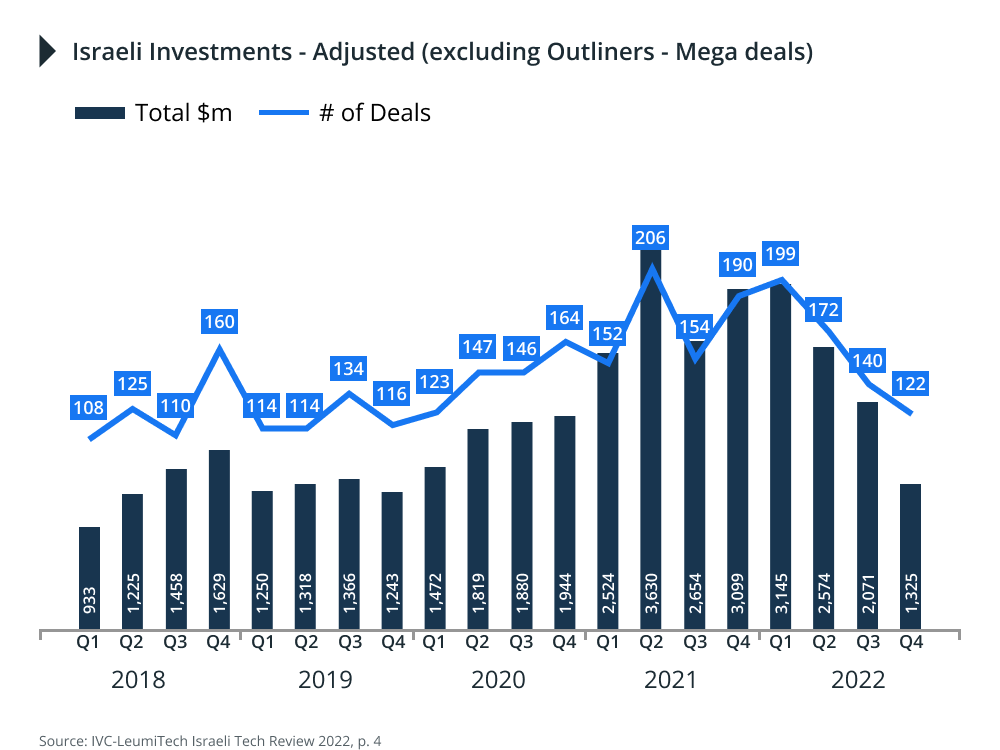

Startup funding

The creator economy is also a source of significant investment from our competitors: creator tools are the fastest growing category of apps, and 50 startups raised at least $2 billion in the first six months of 2021 alone.

Just three city-regions — the San Francisco Bay Area, Los Angeles and New York —account for nearly two-thirds of all global venture capital investment in creator economy startups. But these startups can be found in 65 cities around the world.

Creators are growing and leveraging opportunities

How much creators earn

21% of content creators earn at least $50,000 annually. 1.4% earn over $1 million a year, and another 1.5% make between $500,000 and $1 million. More than two-thirds of creators earn less than $25,000, with more than a quarter earning less than $1,000 per year.

Meta technologies have always provided an opportunity for individuals to shape the content that we can see. Content creators earned $460 million on Instagram in 2022. Online creators earned over $23 billion in 2020.

We split creators into amateurs (46.7 million) and professionals (2 million+). Notably, more than half of amateur creators (30 million) share their creativity on Instagram, followed by 12 million on YouTube, 2.7 million on Twitch and 2 million on other social platforms. In contrast, you’re more likely to find professional creators on YouTube (1 million) than Instagram (500,000), Twitch (300,000) and other platforms (200,000).