Summary of Insights

A Guest Commentary by Viola Ventures, based on data collected by Start-Up Nation Finder.

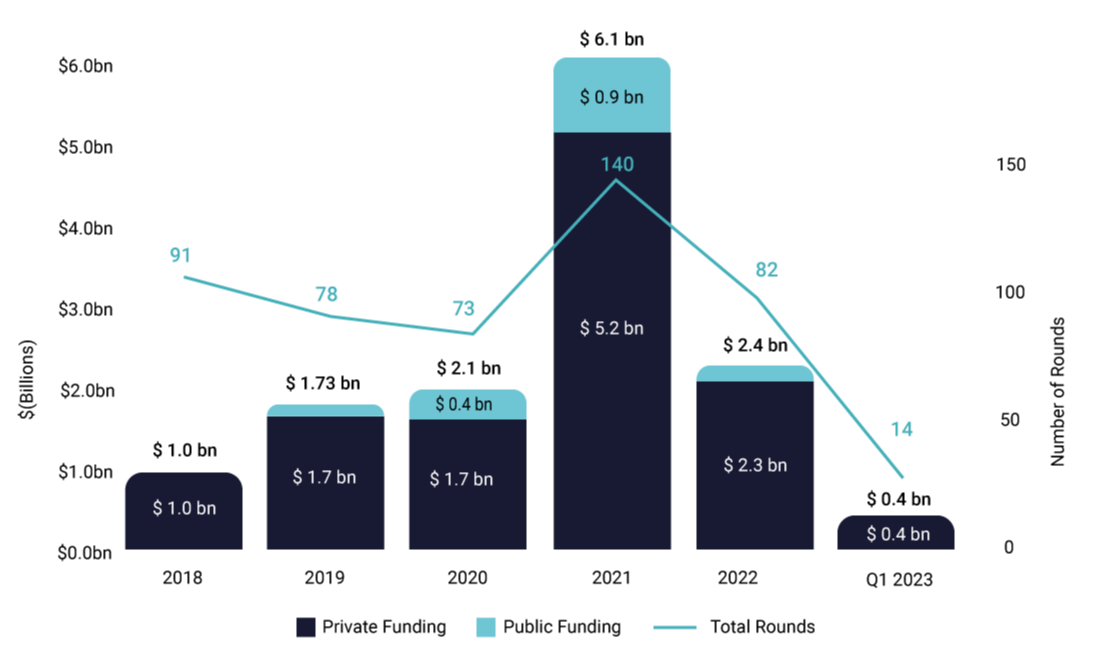

In 2023, the Fintech industry is facing new realities. The higher cost of capital jeopardizes business models that relied on cheap cash. Consumer/business credit models are therefore suffering from higher defaults and lower disposable income/spending.

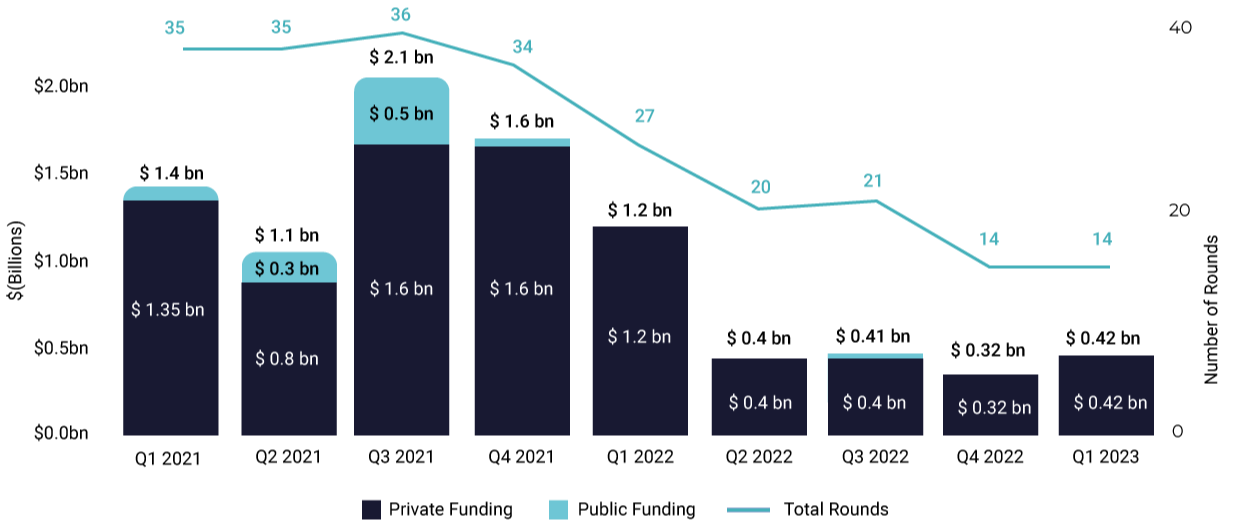

Q1 2023 was de-facto a flat QoQ in terms of number of deals and volume, adjusted for the $250M eToro deal. This represents an ~80% decrease from the peak of the market in H2 2022, consistent with the global trend and other verticals.

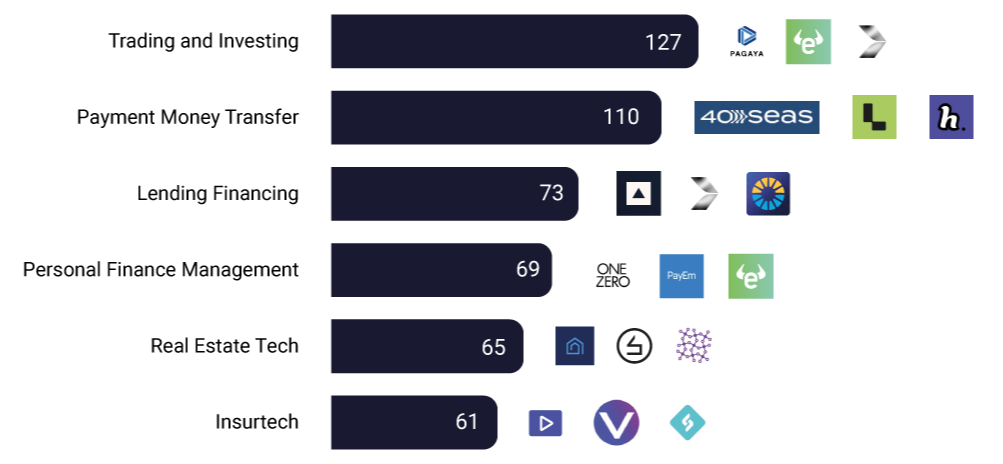

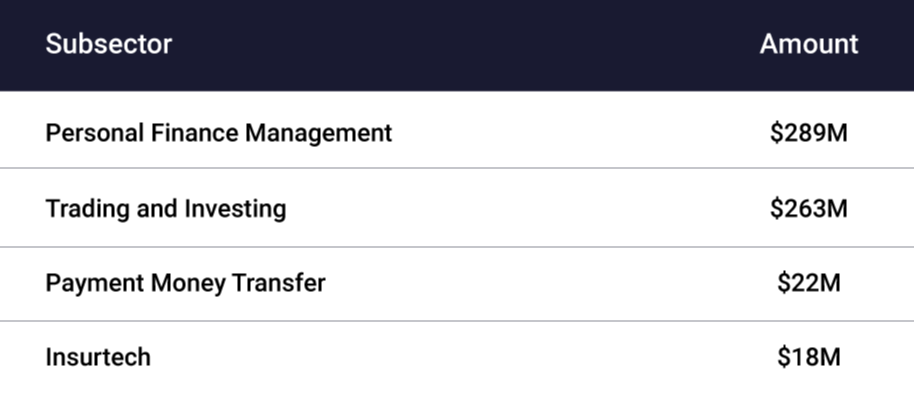

One of the strengths of the Israeli fintech ecosystem is its diversification across subsectors and the agility of builders to pursue new innovative domains. While the bar is higher and the market more selective, we remain excited about the future - mainly around gaps in legacy industries that can be disrupted by leveraging financial services (vertical fintech/embedded finance) and the era of AI-everywhere that is starting to demonstrate a material impact across the financial innovation stack.

Omry Ben David, General Partner, Viola Ventures